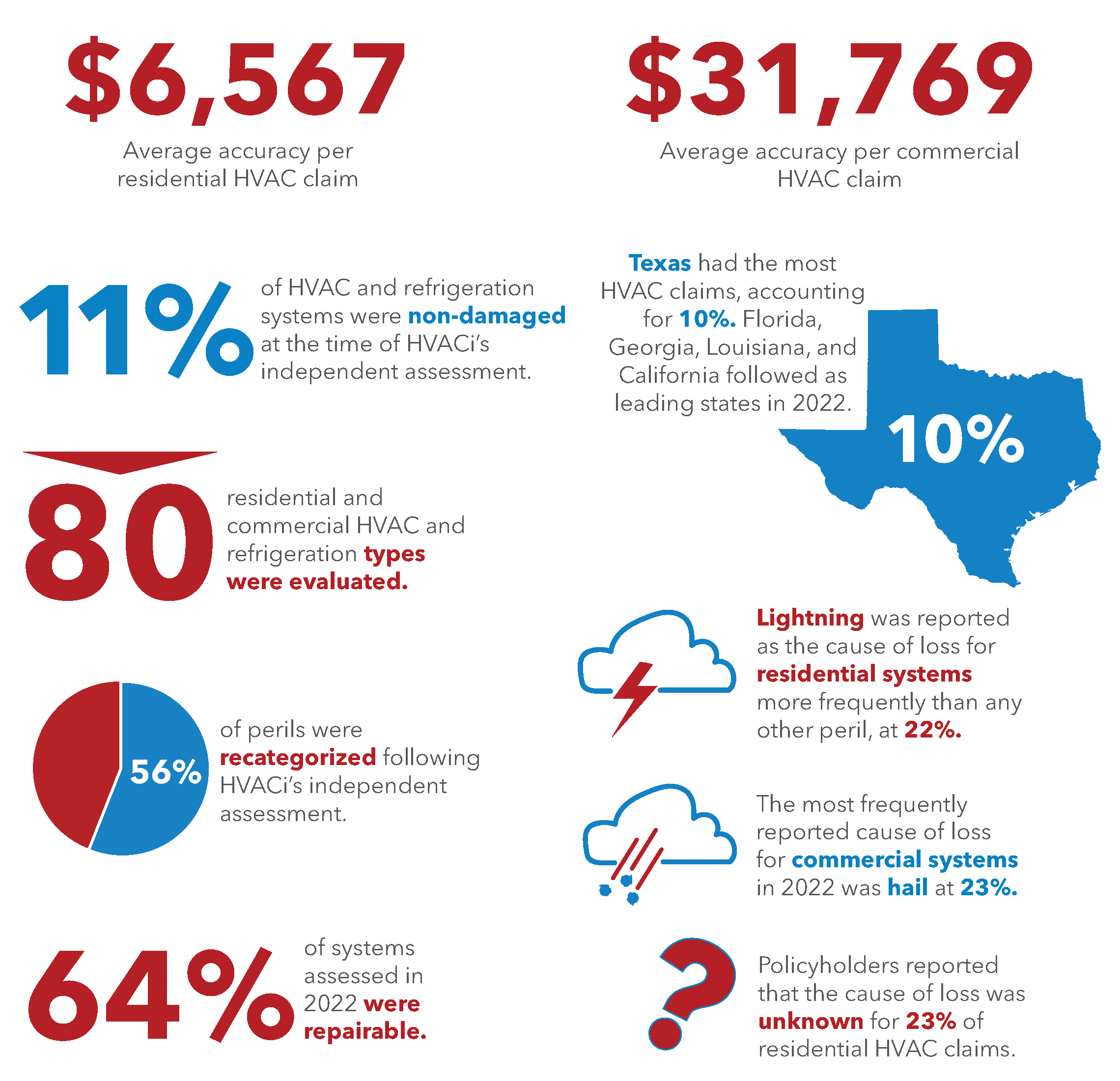

Find out how changes in regulations, parts and labor pricing, and weather may have impacted property claims that included HVAC and refrigeration systems by getting your copy of the HVACi 2022 Annual Claims Report.

This resource geared toward insurance professionals reflects assessment results from nearly 100 different types of HVAC and refrigeration equipment that adjusters nationwide assigned to HVACi’s team in 2022. You’ll gain critical insights and reliable information that can help carriers make more informed decisions, as a whole and on individual claims.

By filling out the form, you’ll be able to review HVACi assessment data about:

Trends related to residential, commercial, and multi-system large loss claims

Reported vs. actual cause of loss data

Percentages of claims by system type, including split systems, package units, boilers, geothermal systems, and more

Reported Hurricane Ian losses and what assessments determined

States that had the most claims

Perils that were reported most often for each month

Average costs of labor and parts

You’ll read which systems were most likely to be damaged by hail, theft and vandalism, high voltage surge, or water. Plus, learn what percentage of equipment was recommended for minor to major repairs or replacements.

Below is just a sampling of the information found in the HVACi 2022 Annual Claims Report.

Rising HVAC equipment and labor costs are increasing prices for insurance settlements.

The following article on “Insurance is not immune to inflation’s impacts,” written by Curt VanNess, Technical Director for HVACi, was originally published on Property Casualty 360.

Cost increases to labor and HVAC equipment are having a trickle-down effect on insurance carriers.

It’s difficult to find many goods or services that haven’t been impacted by inflation. Those effects have trickled down to the HVAC industry, and have extended to manufacturers, contractors, policyholders and insurance carriers.

HVAC manufacturers have reported several reasons for price hikes. Among them are the change in costs in other industries, including for raw materials, and fuel and transportation needs. Insurance professionals may find themselves paying higher settlements to account for the increased labor and equipment costs for both individual components and full HVAC systems. Another consequence is additional claims leakage if the cause of loss and scope of damage aren’t verified before the claim is settled.

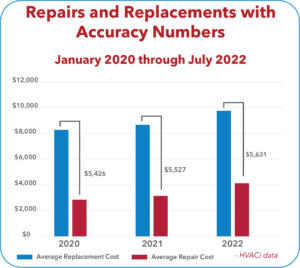

Three-year cost trends on HVAC split systems

Split systems are the most frequently used HVAC system in a home, and they are the second most common HVAC type in commercial claims, according to the 2021 CCG IQ Annual Report.

HVACi, an HVAC and refrigeration assessment company for insurance carriers, tracked the average split system repair and replacement costs over the last three years to note their changes. Between January 2020 and July 2022, each increased, resulting in policyholders and carriers spending more to return equipment to pre-loss condition.

The average split system replacement cost $8,670 in 2021, which was a nearly 5% rise year-over-year from 2020. However, the average split system replacement prices from January through July 2022 jumped to $9,757. Comparatively, in 2021 the average split system repair cost was $3,143, which was a 10% increase from 2020. The average repair cost from January through July 2022 was $4,126 — more than 31% growth.

The average split system replacement and repair costs have only increased since 2020, making the risk of indemnity leakage larger if a carrier settles for replacements in lieu of repairs.

These price changes make it more imperative than ever for adjusters to verify that a split system included in a claim is not functioning as designed, is malfunctioning due to a covered peril, or is unable to be repaired before they settle for a full replacement.

Critical components with price increases

Individual component and labor cost escalations have also made HVAC system repairs more costly.

Condenser coils, which are critical in the cooling process to transport refrigerant and transfer heat to the surrounding air, are susceptible to losses from a variety of perils, including hail and wind. Average costs for HVAC condenser coil repairs increased from less than $2,800 in 2020 to nearly $3,700 by July 2022.

Replacing condenser coils is considered a more minor repair than other alternatives such as getting a new condensing unit to return equipment to pre-loss condition. Still, it may result in unnecessary claims leakage if the original coils could have been cleaned or combed.

HVAC compressors are integral in converting refrigerant from low pressure to high pressure and circulating refrigerant through an HVAC system in cooling mode. Like condenser coils, these also sustain damage from multiple perils and may be replaced to return a split system to pre-loss condition. The average compressor costs increased from $1,592 in 2020 to $2,522 mid-year 2022.

Inflation impacts don’t stop at equipment. Labor prices to make necessary repairs and replacements have also surged. The average total labor cost per claim to repair condenser coils, compressors or control boards was $236 in 2020, and rose to $332 by mid-year 2022.

Compressors are among the critical HVAC components that have seen a price increase in the last three years.

If claims leakage occurs from one of these repairs, a few hundred dollars may not significantly impact the carrier. However, hundreds to thousands of dollars spent on unnecessary repairs and replacements across all claims could have consequences if compounded — and could result in higher premiums or a negative policyholder experience.

The need for accuracy

While inflation has had proven impacts on HVAC claims, adjusters shouldn’t assume settlements must be higher than previously. HVAC system experts can verify the cause of loss and scope of damage and confirm market value pricing to give carriers what they need to accurately settle claims. This results in a better policyholder experience and reduces unnecessary claims leakage, regardless of the inflation rate.

Curt VanNess is the technical director for HVACi. He is responsible for managing the technical team, including HVAC technicians, field managers, and technical writers. Contact him at cvanness@hvaci.com.

Few goods and services have avoided feeling the impacts of inflation, and HVAC equipment is no different. Whether talking about split systems as a whole or individual components, adjusters should take note of how costs have changed and what that means for claims.

Fill out the form to receive your guide on Inflation’s Impact to HVAC System Claims. You’ll receive graphs noting the trends for essential HVAC components over the last three years, data about average labor costs, and information about what insurance carriers can do to reduce indemnity leakage from claims with HVAC systems.

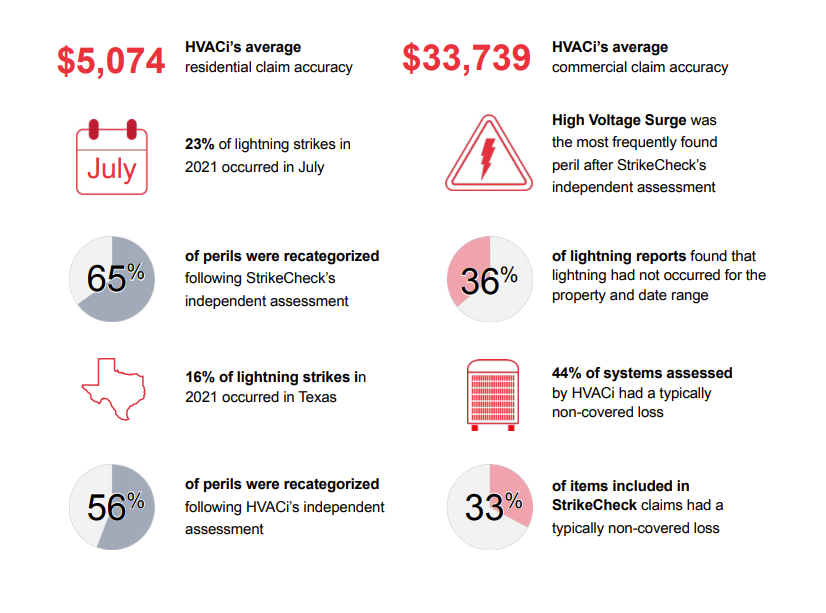

Extreme weather took its toll on property claims in 2021, and more than half of all policyholder-reported perils were recategorized following an independent assessment. The data behind these trends – and others – is available in the CCG IQ 2021 Annual Report.

Experts at HVACi and StrikeCheck, CCG IQ’s damage assessment companies, evaluated hundreds of thousands of items included in claims involving HVAC and Refrigeration systems and electrically powered items.

The CCG IQ team analyzed the results of assessments that adjusters assigned to HVACi and StrikeCheck to provide carriers significant insights about claims nationwide.

Fill out the form to receive your copy of the CCG IQ 2021 Annual Report with data about:

HVAC and Refrigeration Systems: indemnity leakage information, repair vs. replacement frequency, claim data, claim trends by month, and catastrophe data

Electronics and Specialty Items: repair and replacement costs by item type, frequency of claims by item, repair vs. replacement costs, and claim trends by subcategory

Lightning: weather trends by state, lightning report with most found lightning, and the average distance of lightning flashes

Additional Claims Support: the merger between CCG IQ and Donan Engineering offers new opportunities for partnership

Use this resource to make better data-driven decisions related to claims leakage, carrier-wide efficiency and accuracy, and claims resources availability.

The year 2021 may have felt like a blur as the world learned to navigate a new normal left from the swift and lasting effects of the 2020 pandemic. Some of those impacts, among other trends, will continue to take centerstage going into 2022 – and they aren’t all negative.

Technology and Automations Remain in The Forefront

The Pew Research Center studied the use of the Internet during and following the pandemic by surveying U.S. adults in April 2021. The survey found that 90% of them said the internet was essential or important for them personally, and 40% said they used digital technology or the internet in new or different ways.

Policyholders are now using the internet and digital technology more than ever and in new ways – and carriers are taking notice. Photo Credit: “Hands” by Fancycrave1 / CC BY 4.0

Businesses and insurance carriers have also updated their processes to meet customers’ needs through technology. More communication and work can be completed without the need for face-to-face interaction or a personal phone call. For example, automated calls, emails, or texts keep the claim process running more efficiently without unnecessary adjuster touchpoints.

Other virtual amenities include portals and applications for policyholders to use to communicate, check the status of a claim, or quickly obtain information without needing to speak with anyone at the carrier.

These have helped insurance professionals reduce time spent on administrative tasks. Integrations have also made it easier for carriers to obtain the information they need.

Equipment Efficiency Continues to Improve

The U.S. Department of Energy maintains efforts to better equipment efficiency. Manufacturers will likely use 2022 to prepare for the stricter efficiency standards that are expected to take effect for HVAC systems in 2023.

Condensing units in HVAC split systems could need more scrutiny in preparation for efficiency rule changes.

Among the anticipated changes are increases to the standards for the Seasonal Energy Efficiency Ratio (SEER), which is the ratio of total heat removed from a conditioned space during the annual cooling season divided by the total energy an HVAC system consumed during that time. For example, split system condensing units that are less than 3.75 Tons will be required to have a minimum 14 SEER in the North and 15 SEER for the Southeast and Southwest. Additional efficiency requirements are also slated to take effect.

While this impacts manufacturers the most, insurance carriers may need to be prepared to settle for more expensive or upgraded components if replacement HVAC equipment is necessary.

A Crackdown on Insurance Fraud May Be Needed

Insurance fraud, defined by the Insurance Information Institute (iii) as the deliberate deception perpetuated against or by an insurance company or agent for the purpose of financial gain, has long been a concern for carriers. The iii states the FBI has estimated that the total cost of insurance fraud, excluding health insurance, is more than $40 billion a year.

A lack of oversight may be one reason insurance fraud may have increased in 2020. Photo Credit: “Audit” by Tumisu / CC BY 4.0

It is believed the amount of insurance fraud increased during the pandemic because remote work resulted in fewer inspections and workloads changed, which may have caused the amount of oversight to decrease. Other insurance-related fraud included auto and medical bill inflation as well as scams aimed at policyholders through phishing, robocalls, and fake insurance agents.

Insurance professionals should enhance efforts in 2022 to decrease insurance fraud, which is costing carriers and policyholders money through unnecessary settlements resulting in increased premiums.

Third-Party Vendors Support Carrier Goals

In 2022, carriers will likely continue to use time and resources to improve technology, decrease insurance fraud, and ensure the most accurate settlements are being made.

HVACi is committed to helping carriers reach their goals by being their expert assessment source for property claims related to HVAC and Refrigeration equipment. Onsite assessments provide a comprehensive evaluation to decrease insurance fraud and unnecessary settlements for equipment working properly or damaged by non-covered losses. Improved technical initiatives keep the claims process moving quickly without sacrificing accuracy. Lastly, our knowledgeable team keeps up with changing regulations that could impact claim results so that insurance professionals don’t have to.

Go into 2022 knowing that you have the support you need to keep technology at the forefront, be part of the movement to improve efficiency, and take a stand against insurance fraud. Find out more about HVACi’s services or submit a claim for an accurate solution.

For years CCG IQ’s damage assessment brands, HVACi and StrikeCheck, have been publishing separate annual claims reports to equip carriers with data-driven facts and trends to help them control claim leakage and keep a superior policyholder experience. This year, all of CCG IQ’s suite of services, including claims assessments, underwriting inspections, and lightning verification, are highlighted in the CCG IQ 2020 Annual Report. This offers an enhanced overview of a broader spectrum of risks and perils that impact a carrier’s overall book of business for better decision-making.

Fill out the form to receive key insights into perils and hazards that have affected policies throughout their life cycle. The data reflects the thousands of claims, underwriting, and lightning assignments CCG IQ completed in 2020 using technology and experience to provide insurance carriers objective, knowledgeable, and timely policy solutions.

The report includes:

Reported vs. actual cause of loss, repair and replacement costs, and frequency of claims by item type for HVAC systems and all electrically powered items

Claim trends for time of year, states, and claimed amounts

Catastrophe claim data

Lightning data by month, location, and frequency

Average coverage amount vs. replacement amounts

Frequency of certain home characteristics, roof problems, and property features

States with the highest potential for hazards

Plus, a demonstration of how claims, lightning, and underwriting data can be combined for better decision-making about a specific region

Review the annual report and consider how CCG IQ can support your carrier’s efforts to increase carrier efficiency and improve claims leakage and loss ratios.

Just the Facts is HVACi’s tagline for a reason. It’s something we believe in and achieve from the moment insurance personnel put their trust in us to handle their assessments for claims related to HVAC systems all the way until we provide them final reports with our recommended claim resolutions.

HVACi operates using its proven process to ensure accuracy and objectivity for every claim. Among the ways we do that are by selecting experienced personnel, staying current with industry best practices and regulations, and peer reviewing our work to avoid error. These methods guarantee that we base our recommendations on facts to empower adjusters to make accurate and fair settlements for their policyholders.

Choosing Qualified Personnel

Our technicians are our eyes and ears at an insured’s property, thus we verify the people we send have the necessary skills and experience to perform the assessment. To even be considered for a job, technicians must have at least 5 years of experience, an EPA Type II or Universal Certification, and a valid state and local HVAC contractor’s license if required by area jurisdictions. We follow up to make sure these qualifications are kept up to date. They must also pass technical exams. We have an additional measure of requiring all technicians to pass criminal background checks. These steps help certify that the technicians have expert knowledge of the equipment they’ll be assessing and will maintain the high level of customer service you have come to expect from us.

Technicians must also follow HVACi guidelines against soliciting work from the insured. That includes trying to promote their businesses to make the needed repairs or replacements related to that particular claim or any future ones. Technicians are also not allowed to discuss their findings with the policyholder. As HVACi only recommends claim solutions and doesn’t have any decision-making authority, it would be inappropriate for anyone other than the adjuster to discuss the claim with the insured.

Our company’s technical team has hundreds of years of contractor field experience and forensic technician experience. The technical team’s knowledge base in documenting inspections, servicing equipment, and repairing and replacing systems in both residential and commercial environments is what sets us apart in keeping to just the facts.

Staying Current with Industry Best Practices and Regulations

HVACi staff is cognizant that the industry has undergone changes as new products are released and new regulations are announced. Even with our wealth of experience, it’s impossible to stay accurate without continued education and staying up to date on trends, best practices, and rules.

We work hard to stay informed. And since we’ve done the homework for you, we want to share our knowledge. Adjusters and other insurance personnel know to come to us when they have questions about various HVAC-related topics, including refrigerant regulations, even if their insured’s claim has been closed. We also regularly provide updated articles and resources as well as host webinars to teach others about the complex equipment we deal with daily.

Peer Reviews for Accuracy

Qualified personnel write each report for the assessments, but we don’t leave room for error.

Each claim assessment goes through a multi-level process, including peer reviewing, prior to being delivered to the adjuster. We analyze the data and draw conclusions before communicating our results. These are then peer reviewed for errors to make sure our final reports are polished and mistake-free. We also ensure our labor and equipment estimates are backed by industry standards and current values, thanks to our access to manufacturer databases.

Plus, if there are any follow-up questions, we have a resolutions team willing to reopen the claim file and offer more insight.

Going Forward

Next time you see our logo and the phrase “Just the Facts,” know that we wouldn’t have it any other way. Just the Facts incorporates HVACi’s commitment to knowledge, accuracy, and objectivity and is not just a saying – it’s our way of doing business.

CHARLOTTE, North Carolina, February 26, 2020 – StrikeCheck, the leading provider of electronics damage assessments for Property & Casualty insurance carriers nationwide, announced the release of its 2020 Annual Claims Report today. The report features statistics that can help carriers make data-driven decisions and highlights areas where they can improve claim leakage control.

The 2020 Annual Claims Report is distributed to insurance carriers throughout the country. It summarizes data from thousands of residential and commercial claims in all 50 states that were referred to StrikeCheck in the previous year. The report examines claim trends in multiple electrical equipment categories from all causes of loss. Lightning was the most frequently claimed peril in 2019, with TVs and refrigerators as the top claimed electronic items. The 2020 Annual Claims Report also spotlights larger equipment such as solar panels, generators, pool equipment, well pumps, water heaters, electrical systems, and other high-value items that are critical to fully investigate, as they are often repairable.

In addition, the report includes the standard information that carriers have come to rely on, such as reported vs. actual cause of loss, average age of equipment, repair vs. replace cost comparisons, and claimed perils by month. New for 2020 are data points on commercial-specific items, year-over-year changes, and property type trends. As carriers continue to navigate new and changing technologies, these statistics clearly illustrate the need to partner with an expert vendor to control claim leakage, without negatively impacting the customer experience.

“Connected devices are changing the insurance landscape from both a claim and a risk perspective,” says CCG IQ (parent company of StrikeCheck) CEO Damon Stafford. “The data available presents a significant opportunity for carriers to make faster and more informed decisions, and we’re committed to helping organizations use these insights to create a better policyholder experience.”

StrikeCheck, a CCG IQ company, investigates electronic and specialty contents claims exclusively on behalf of insurance carriers, nationwide. We boast the industry’s broadest range of manufacturer relationships and extensive experience across thousands of investigations annually, delivering cost-effective, comprehensive solutions for complex claims. To learn more about our services or to submit an assignment, visit strikecheck.com, email claims@strikecheck.com, or call (888) 980-8544.

This education is brought to you by our sister company StrikeCheck.

Carriers Have Opportunity to Uncover Hidden Risks and Potential Claims Leakage to Better Understand Their Business

HVACi’s 2020 Annual Claims Report provides carriers with data on thousands of actual claims

CHARLOTTE, North Carolina, February 12, 2020 – HVAC Investigators (HVACi), the nation’s leading provider of HVAC Refrigeration damage assessments for Property and Casualty (P&C) insurance carriers, announced the release of its 2020 Annual Claims Report today. The report provides an analysis of actual 2019 claim data and offers carriers compelling insights into risk management and claim leakage control.

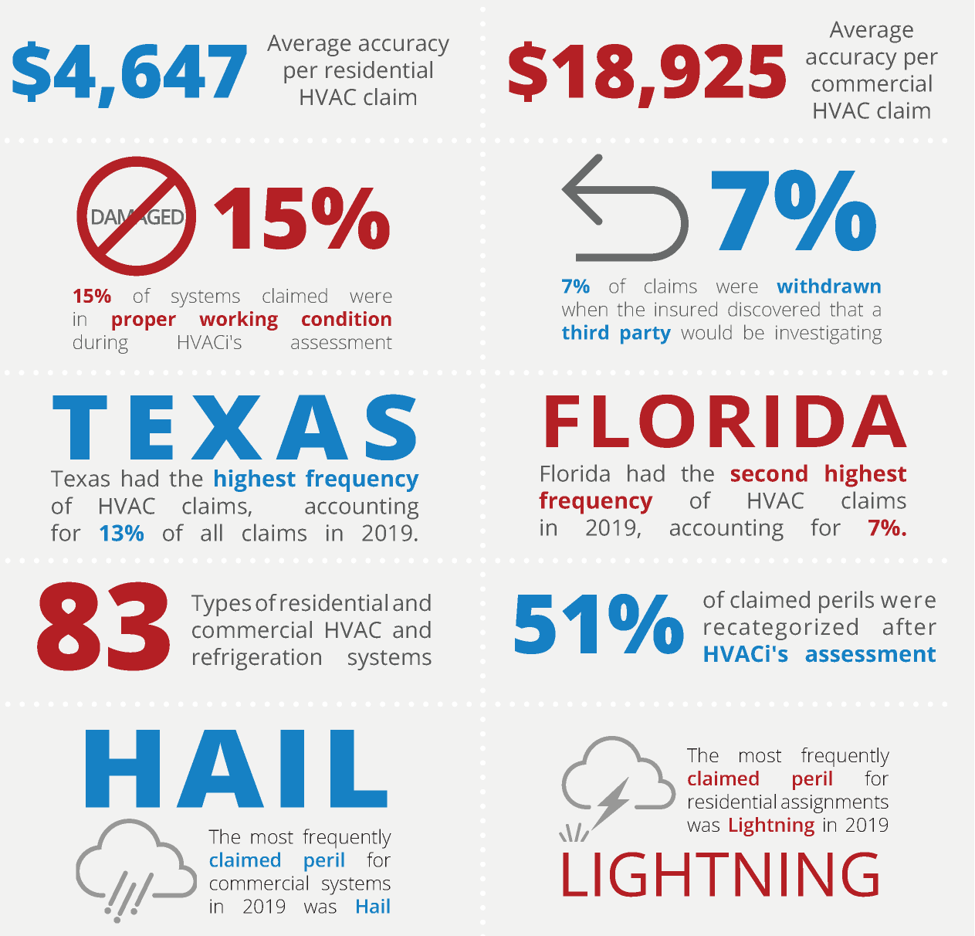

Consistent with previous reports, this year’s findings once again illustrate the critical need for carriers to partner with a third-party expert to evaluate HVAC losses to better control indemnity leakage. For example, as the report notes, 51% of claimed perils investigated by HVACi were recategorized, with 15% of all claimed systems found in proper working condition at the time of the independent assessment. Furthermore, carriers that used an objective, third-party firm realized on average $4,647 in accuracy per residential HVAC claim and $18,925 in accuracy per commercial claim.

This report is compiled annually from many thousands of claims referred to HVACi by the nation’s top carriers in all 50 states. It is distributed at no cost to P&C insurance carriers nationwide to help fulfill HVACI’s mission of providing transparent data to improve the insurance industry.

The 2020 report delves into each policy line to provide a thorough analysis for carriers to compare with their own policy data. Additionally, the report highlights five-year trends and spotlights some of the largest catastrophes of 2019. It also covers popular topics that carriers have come to rely on, including repair vs. replace frequency, reported vs. actual cause of loss, distribution of claims by state, and frequency of claims by system type. New additions to this year’s report include expected values for residential and commercial systems; data trends compared with the previous year’s analysis; and cumulative peril trends. These data points can help carriers to better understand risks hidden in their policies, make efficient resource management decisions, and set appropriate indemnity reserves.

According to Damon Stafford, CEO of CCG IQ, HVACi’s parent company, “Our Annual Claims Report offers carriers an opportunity to review their own policy and historical claims data to see where they may have hidden risks or a potential to better understand their claim exposure. I hope they use this data analysis as a tool to make better underwriting and claims decisions.”

HVAC Investigators (HVACi) is the nation’s leading provider of HVAC and refrigeration damage assessments and part of the CCG IQ group of companies. Our prompt inspections, actionable reports, and national footprint help insurance carriers settle HVAC claims more quickly and with a higher degree of accuracy. To learn more about our services or to submit an assignment, please visit hvaci.com, email info@hvaci.com, or contact us by phone at (888) 407-5224.

As the nation’s leading provider of HVAC and Refrigeration damage assessments, HVACi is committed to highlighting the significant opportunity for insurance carriers to control claim leakage without forfeiting the essential customer experience. Our Annual Claims Report features data cultivated from thousands of residential and commercial claims assigned to HVACi by the nation’s top insurance carriers in all 50 states. This year’s report illustrates the prevalence of HVAC claims in the insurance industry and the value in engaging third-party experts to capture powerful results.

To view the full report, fill out the form provided.

Policyholders are now using the internet and digital technology more than ever and in new ways – and carriers are taking notice. Photo Credit: “Hands” by Fancycrave1 / CC BY 4.0

Policyholders are now using the internet and digital technology more than ever and in new ways – and carriers are taking notice. Photo Credit: “Hands” by Fancycrave1 / CC BY 4.0 Condensing units in HVAC split systems could need more scrutiny in preparation for efficiency rule changes.

Condensing units in HVAC split systems could need more scrutiny in preparation for efficiency rule changes.  A lack of oversight may be one reason insurance fraud may have increased in 2020. Photo Credit: “Audit” by Tumisu / CC BY 4.0

A lack of oversight may be one reason insurance fraud may have increased in 2020. Photo Credit: “Audit” by Tumisu / CC BY 4.0