Adjusters, Ensure Accurate HVAC Claims Settlements By…

Settling claims fairly and accurately begins with making sure you as an adjuster have all the necessary information from the start and that it’s verified. This includes determining cause of loss, scope of damage, and appropriate repair or replacement recommendations priced at market value. Anything less means the claim settlements could be for an inaccurate amount.

Adjusters, ensure your claims with HVAC systems are settled as accurately as possible by:

1. Considering all repair options rather than only full replacements

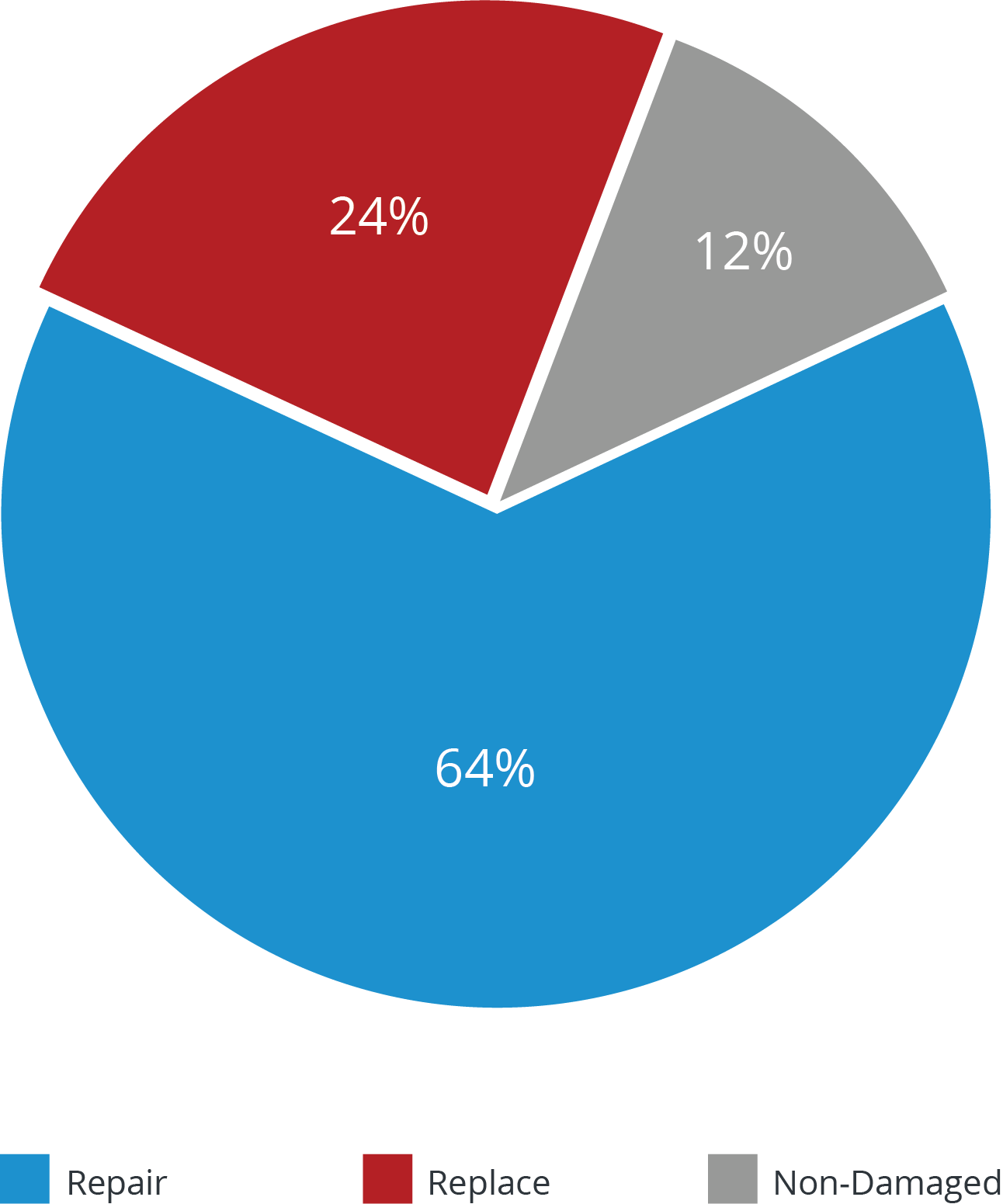

The percentage of residential HVAC systems that required a full system replacement totaled less than a quarter of all the systems HVACi assessed last year.

The percentage of residential HVAC systems that required a full system replacement totaled less than a quarter of all the systems HVACi assessed last year.

Contractors often like to tell your insureds that a full HVAC replacement is required to return them to pre-loss condition. They might use reasons such as, “Repairing an HVAC only extends its lifetime by a year or two” or that “Replacements will save you money in the long run.” Justifications exist for why a replacement may be necessary, including if there is a safety hazard or if the cost of repairs is more expensive than installing a new system. But full replacements are usually not the best solution, and most settlements don’t require one.

Repairs, including swapping out a major component and leaving the rest as it is, are more likely than replacements. The HVACi 2020 Annual Claims Report states only 24% – less than a quarter – of residential HVAC systems were determined to need a full replacement. It’s important adjusters have an equipment evaluation completed to see if an alternative is available that would be a more accurate and appropriate solution.

If you’re settling for more replacements than repairs, you’re likely adding unnecessary claims leakage.

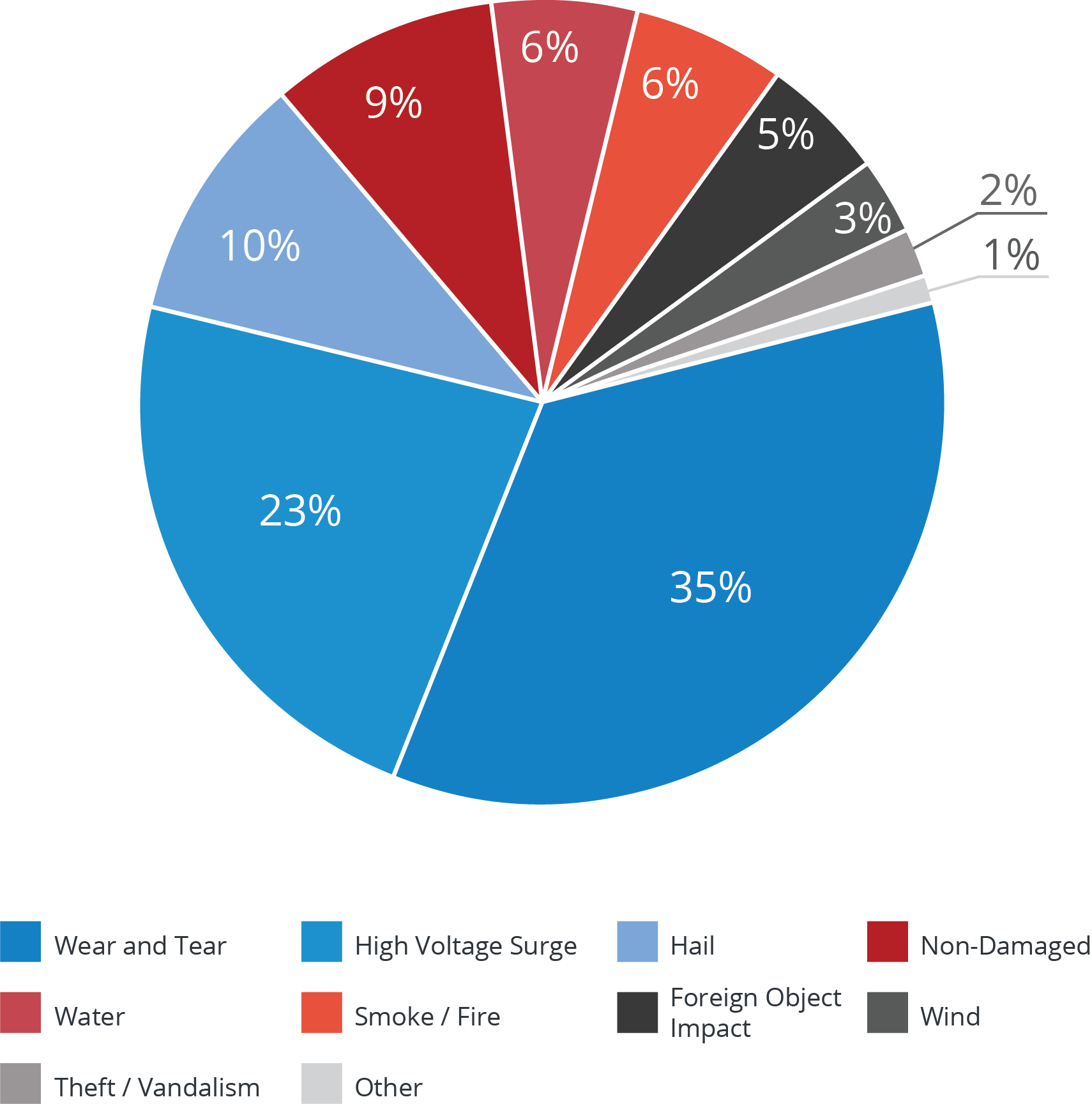

2. Confirming cause of loss

HVACi’s assessments determined these were the actual causes of loss for residential split systems. Policyholders more often had them claimed as a different peril, which could have resulted in settlements for damages that shouldn’t have been covered.

Lightning, hail, and water are all perils that affect HVAC systems and were the most claimed causes of loss outside of “unknown” on residential HVAC claims last year. However, HVACi assessments determined these perils were not actually the most common causes of loss impacting residential split systems, as shown by the graph above. It’s important adjusters determine why the equipment sustained damage to ensure they’re making accurate settlements for only the perils covered by the policy.

More than half of the residential systems HVACi assessed were recategorized to a peril other than what was claimed after evaluation. For residential split systems, more than a third were determined to be damaged because of age-related wear and tear.

If you’re settling most HVAC claims without verifying cause of loss first, you likely have had inaccurate settlement results.

3. Assessing each unit in claims with multiple HVAC systems

Thorough testing should be completed on all equipment, regardless of how many systems are included in each claim.

Thorough testing should be completed on all equipment, regardless of how many systems are included in each claim.

Commercial and large loss claims frequently have multiple systems included in them with a costly claimed amount. To get the most accurate results, adjusters should have thorough evaluations of each item – even if there are hundreds.

Nearly 20% of the commercial HVAC systems evaluated last year were determined to be non-damaged at the time of assessment. One-third of all commercial systems didn’t sustain covered losses and shouldn’t have been included in the claim.

If you’re not assessing every HVAC system included in claims, you’re probably settling for equipment that wasn’t damaged or was damaged by a peril that isn’t covered by the policy.

4. Verifying market pricing and availability

Not double-checking equipment estimates could result in settlements that are higher than they should be. Photo Credit: “Accountant” by Shutterbug 75 / CC BY 4.0

Not double-checking equipment estimates could result in settlements that are higher than they should be. Photo Credit: “Accountant” by Shutterbug 75 / CC BY 4.0

Contractors provide policyholders estimates based on their company’s pricing, which may not be in line with market costs. An adjuster should verify scope of damage and the cost of equipment and labor to make the most accurate settlement.

Real facts should be the foundation for a settlement cost – not overinflated equipment estimates. The expense for materials should be based on market value pricing. Labor costs should be consistent with the loss location.

If you aren’t verifying market pricing, you might be settling for more than necessary.

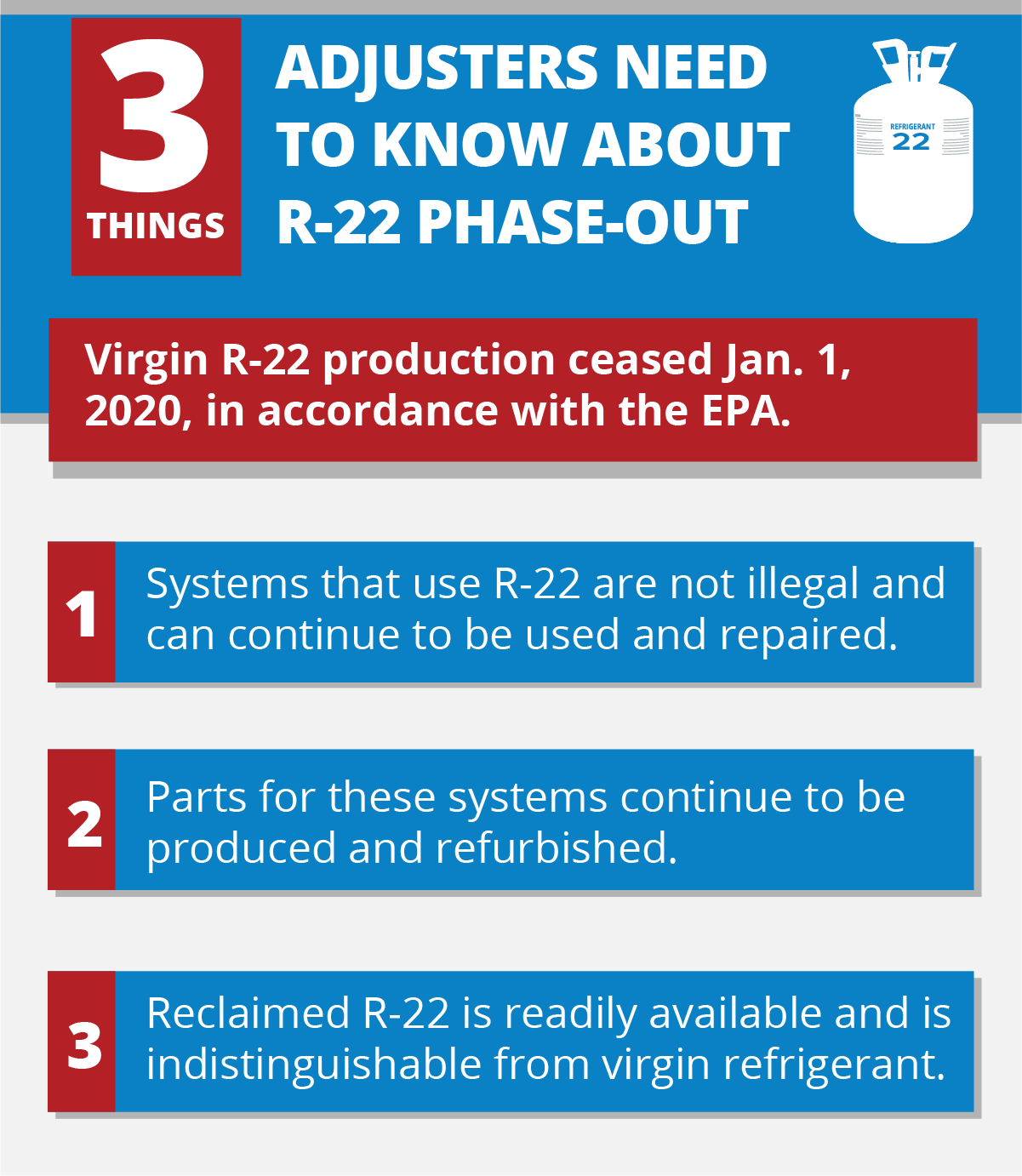

5. Being up to date on regulations and exactly what they mean

Policyholders, contractors, and adjusters may misunderstand changing regulations or believe untrue or misleading information about them. It’s important to know exactly what they entail to make accurate settlements.

Policyholders, contractors, and adjusters may misunderstand changing regulations or believe untrue or misleading information about them. It’s important to know exactly what they entail to make accurate settlements.

January 1, 2020, was an important date in the HVAC industry. That’s when the phase-out of new production of R-22 ceased entirely and only reclaimed R-22 became available on the market. The news of the deadline came years in advance and so did the start of myths surrounding the phase-out. An adjuster who isn’t up to date on regulations could fall victim to a contractor who doesn’t fully understand the rules or is banking on no one else knowing them and unnecessarily approving a full replacement “in order to comply.”

Energy efficiency regulations, including SEER standards, and other federal and local codes impact how equipment may be manufactured, repaired, or replaced. It’s important adjusters stay familiar with how their policyholders and their claims could be impacted.

If you aren’t up to date on regulations and what they mean, you may not be settling claims accurately.

6. Using a knowledgeable, objective third-party assessor

Many adjusters rely on third-party assessment companies to evaluate their policyholders’ HVAC systems. This is a good idea if it’s a company you know will offer objective, comprehensive, and accurate assessments based on just the facts.

HVACi is the nation’s leading provider of HVAC and Refrigeration damage assessments thanks to its thorough investigations, swift cycle times, and actionable reports that enable insurance carriers to settle claims quickly and accurately. Our experienced and knowledgeable professionals verify cause of loss, assess every HVAC system and component listed on the claim, and provide replacement and repair recommendations. Each report also includes market pricing and equipment availability to ensure you are settling for the appropriate component at a fair and accurate price. Plus, HVACi’s subject matter experts not only stay up to date on trends and industry news, they also offer continuing education training and educational resources for adjusters.

Don’t run the risk of settling any claims inaccurately because it could lead to a negative customer experience or unnecessary claims leakage. Submit a claim to HVACi to receive an accurate claims assessment that will lead to better settlements and resolutions.