A small kitchen fire, a furnace blaze, or a wildfire raging miles away could all impact policyholders’ residential and commercial HVAC systems and result in an insurance claim. Some HVAC equipment can also actually intensify the damage by circulating smoke and other elements throughout a property.

However, these claims don’t always require a full replacement to return a policyholder to pre-loss condition. In 2019, nearly 50% of the HVAC systems that HVACi evaluated for smoke and fire damage could be repaired or were in proper working condition at the time of inspection.

We’ve put together an adjuster toolkit to better prepare you for fire or smoke damage claims with HVAC components. Fill out the form to receive each of the listed resources, including articles, guides and video, that provide a brief overview of components that could be affected by smoke and fire as well as potential repair and replacement considerations.

Content included in the kit:

Know How Smoke and Fire Impact HVAC Systems Guide

HVAC Smoke and Fire Damage Guide

Don’t Forget HVAC Repairs for Smoke and Fire Claims

Smoke and Fire Damages to HVAC Systems Webinar Recording

Lightning and voltage surges get blamed for everything in the claims world. And while the damages they produce have earned them a negative reputation, they frequently aren’t the actual cause of loss. This reiterates why an expert should assess if and why equipment sustained damage and what it would take to return the policyholder to pre-loss condition.

Just ask the adjuster in this edition of Scary Story, who was handed a claim for a damaged boiler that was estimated to have a replacement cost of nearly $10,000. That’s a lot of potential claims leakage if a replacement isn’t warranted. Fill out the form to learn more about the “surge” that caused the boiler to malfunction, why it occurred, and what HVACi recommended the adjuster and the policyholder do about it.

The Hail Claims Involving Residential and Commercial HVAC Systems Webinar has already occurred. You can watch the recording here.

Be more familiar with which HVAC components are susceptible to hail damage and what measures can return your policyholder to pre-loss condition during HVACi’s Hail Claims Involving Residential and Commercial HVAC Systems Webinar. Find out the significance of hail damage in insurance claims, ways to identify if cause of loss is hail or another peril, and repair options that could be available.

During the webinar, we’ll review:

The significance of hail damage to HVAC systems

Components frequently damaged by hail

Signs of hail damage to residential and commercial HVAC systems

Real-life residential and commercial hail claims

Potential repair options

Important: Pre-recorded webinars do not qualify for CE credit.

With snow piling up and outside temperatures below freezing, a policyholder in New York doesn’t want to worry about the boiler not working during the winter months. But then there is a bang, and it smells like soot near the boiler. The insured just lost a method to heat their home, and an adjuster will now receive a claim for a damaged boiler.

Insurance adjusters should be familiar with the causes of most boiler damages – including puffbacks, low water cut off malfunction, surges, theft, and water – to understand why it’s critical to assess the equipment before settling a claim. Many of these damages fall under the category of wear and tear, which isn’t typically covered in an insurance policy and accounted for 44 percent of the boilers in claims HVACi assessed last year.

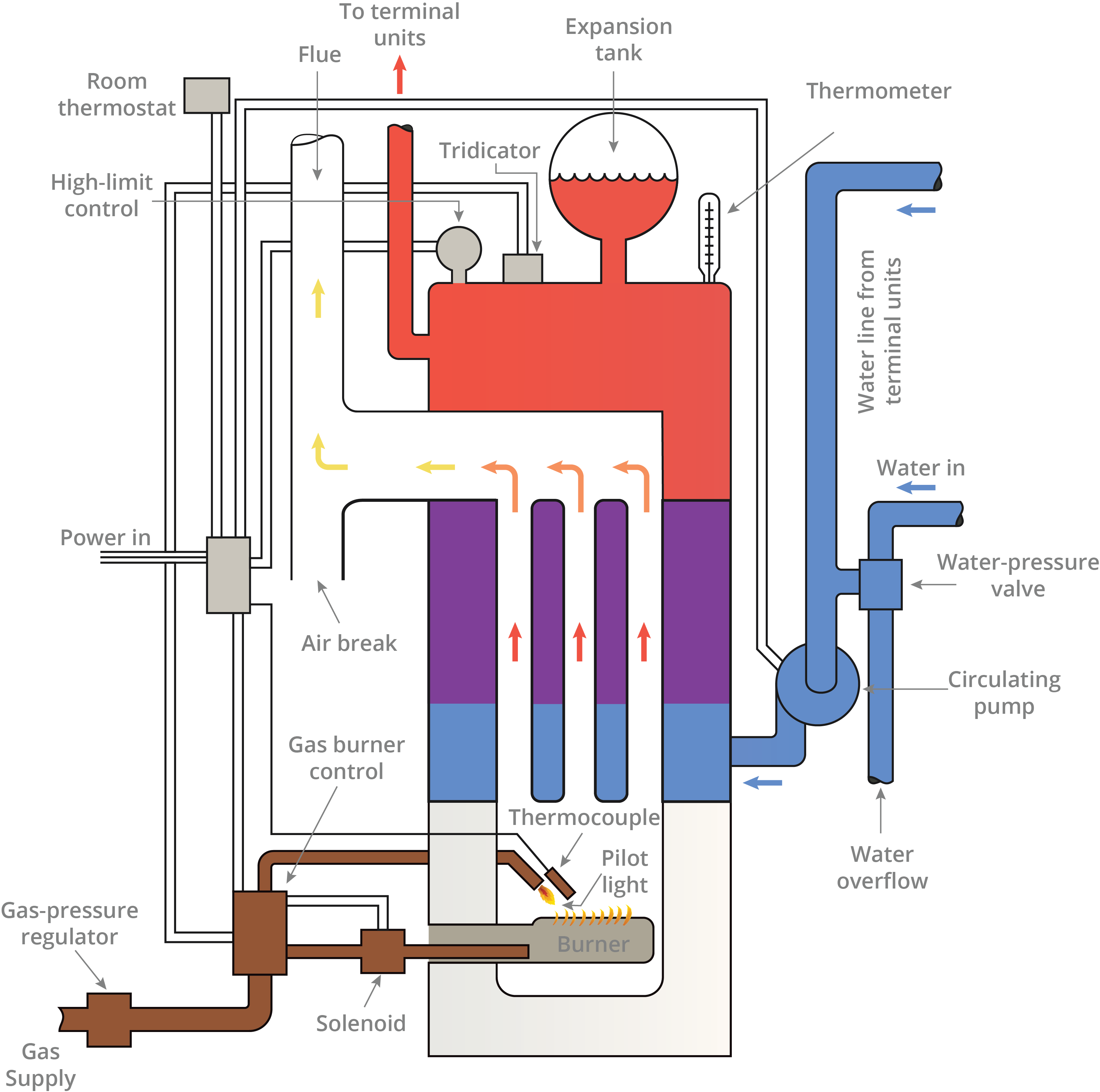

Boilers Rely on Water To Distribute Heat Evenly

Boilers have a variety of equipment used to heat water or steam that is transferred via pipes and terminals, including radiators and non-electric baseboard registers, to warm a home or business.

Unlike a furnace that delivers heated air through ductwork and vents, boilers are hydronic systems that distribute steam or hot water throughout buildings to provide heat via pipes and terminal units. Water or steam radiators, non-electric baseboard registers, and underfloor tubing hydronics systems are among the terminals used.

Boilers are commonly fueled by natural gas, which burns cleanly and comes from an installed natural gas line, or by oil, which requires a large onsite tank. Propane can also fuel boilers, though it is mainly used in areas where oil is not common or where there is no natural gas service. Another option, though also more rare, are wood-burning boilers. Boilers that run on oil can cost double or triple the price of one that uses natural gas, though a boiler’s efficiency and size can affect equipment and installation totals for either type.

The kind of boiler and the types of terminal units being used can affect which peril is more likely to occur.

Puffbacks Occur Following Fuel Buildup – And Poor Maintenance

An insured hearing a bang from the boiler may be an indication a puffback has occurred. Something has caused an oil or gas buildup within the heat exchanger, and the excess fuel produces smoke when it ignites. Puffbacks are more likely to occur in oil-fueled boilers because these types of systems need to be serviced more frequently and excess oil is less likely to dissipate than natural gas.

Triggers for this include: a leak causing fuel to build up in the heat chamber; accumulated gas or oil from manually resetting the system too often when it fails to ignite; an exhaust or flue that is clogged by dirt, dust, fuel residue, rust, or corrosion; a cracked heat exchanger; a clogged or cracked oil fuel nozzle that causes oil to spray unevenly into the burner; or a clogged burner full of dirt, dust, fuel residue, rust, or corrosion that causes a misfire and allows for fuel to build up in the combustion chamber.

Because turning a system back on after a puffback isn’t recommended, HVAC professionals can test a system by checking for fuel leaks, examining the flue for clogs, holding a candle near the heat exchanger while the blower is on to detect a crack, and inspecting the oil nozzle and burner assembly.

Puffbacks can be costly and even dangerous for a policyholder, but they are typically the result of poor maintenance and age-related wear and tear.

Low Water Cutoff Malfunctions Send Wrong Messages to A Boiler

Low water cutoffs can be clogged by Total Dissolved Solids in the supply water, which could cause them to send wrong messages to the boiler and either run without an adequate water supply or shut off unnecessarily.

Water is integral to a properly functioning residential or commercial boiler, and it’s important an adequate supply is available. Low water cutoffs are meant to turn off a boiler if there isn’t enough water to transfer heat to, but they can also malfunction and cause further damages by sending the wrong message.

Low water cutoffs can be electronic or mechanical. Mechanical is the most widely used water-level safety device, but it is also the switch more likely to fail. A properly working mechanical low water cutoff has a float that stays at the surface of the water. When the water level increases, the float valve goes up, and when the water level drops, the float valve lowers with it. When water gets to an unsafe low level, the boiler shuts off.

Supply water has Total Dissolved Solids (TDS), including minerals, dirt, and rust, that build up over time. Too many TDS could cause the mechanical-float low water cutoff to get stuck and prevent it from moving with the water level. If the water level became too low, the boiler wouldn’t automatically shut off.

Foaming water can keep a mechanical float higher than the actual water level. If the water level decreases too low, the foam could inhibit the mechanical float from recognizing the drop and shutting off the boiler.

In both situations, the malfunctioning low water cutoff could allow the boiler to run without water, which is called a dry fire. The heat generated in the boiler’s combustion chamber cannot transfer the heat to the water, and instead, the heat exchanger and boiler tubes overheat. If this happens for too long, the metal walls of the burner, boiler, or heat exchanger can weaken and crack. This could lead to a fire, explosion, or, in most cases, a leak from water escaping via the crack.

Cold temperatures could cause the circulation pipes for the boiler to become frozen, which will keep the system from receiving an adequate water supply. If the low water cutoff malfunctions at the same time, this could also result in dry fire.

On the other hand, a water-logged float could sink to the bottom regardless of the water level. This sends the message that the supply is too low and unnecessarily shuts down the boiler.

Like a puffback, failures of a low water cutoff switch point to a lack of regular maintenance or age-related wear and tear. To prevent any malfunctions, TDS should be removed by regularly flushing the low water cutoff valves. Boiler feedwater should also be chemically treated to prevent scaling and maintain proper pH levels. Low water cutoff equipment is less expensive to purchase, install, and maintain when compared to the catastrophic damage that can occur from dry fire.

Surges Affect A Boiler’s Electrical Components

Lightning and high voltage surges are among the perils that can damage a boiler system’s electrical components, including the thermostat.

High voltage surge is a voltage fluctuation that can lead to overarching electrical damage. Surges affected 10 percent of the boilers HVACi assessed last year because they can impact the boiler’s electrical components.

Thermostats can be digital or use smart technology to make them easier to set to a desired temperature. They signal the burners to ignite to warm the boiler’s heat chamber. Other electronic boiler components can include an electronic low water cutoff or an electronic ignition that doesn’t require a pilot light. Additional components that could malfunction from surges are aquastats, circulating pumps, and some electronic zone control valves.

If a boiler is fully electric it can be at risk for more damages from surge. These do not use any other fuel source to generate steam to heat a facility and are more efficient, according to the U.S. Department of Energy; however, the cost of electricity makes all-electric boilers too expensive.

Similarly to the impacts of surges on consumer electronics, electronic boiler components should be evaluated by a professional following a voltage irregularity and could require replacement.

Water and Freezing Damage Boilers and Property

Boilers have gas valves and burner assemblies that are among the equipment that can be damaged when submerged by water.

As critical as water is to a boiler system, it can also be the cause of major damages.

Elements affected from prolonged water exposure are the electrical components, burner, and the combustion or heat chamber. If the system or components got wet during a loss, the system should be evaluated by an HVAC professional for potential damages or issues related to water damage.

Policyholders sometimes opt for an underfloor hydronics system, which uses pipes between the slab or subfloor and finished flooring to heat a room. Leaks in a pipe may be difficult to detect until major water damage has occurred.

Freezing, another peril that damages boilers, causes pipes, terminal units, or valves to burst and results in water damage. Repairs may be difficult depending on what metal was used in the pipes. Copper is easier to repair, while cast iron may need to be replaced.

Theft Is Rare, But It Does Occur

Only 2 percent of the boilers in claims HVACi assessed had theft and vandalism as the cause of loss, but it can happen. Copper is a popular metal to steal, particularly from HVAC equipment. The theft of copper piping in boilers could damage other components and wires that will need evaluation.

Theft, water, surges, puffbacks, and low water cutoff malfunctions are all damages that need a trained eye to accurately confirm cause of loss and scope of damage. By not doing that, adjusters risk settling for a peril that isn’t covered by a policy or paying for replacements that aren’t necessary.

HVACi is the nation’s leading provider of HVAC and Refrigeration assessments for insurance carriers. Adjusters should submit a claim to receive comprehensive and objective claim handling solutions in a timely manner.

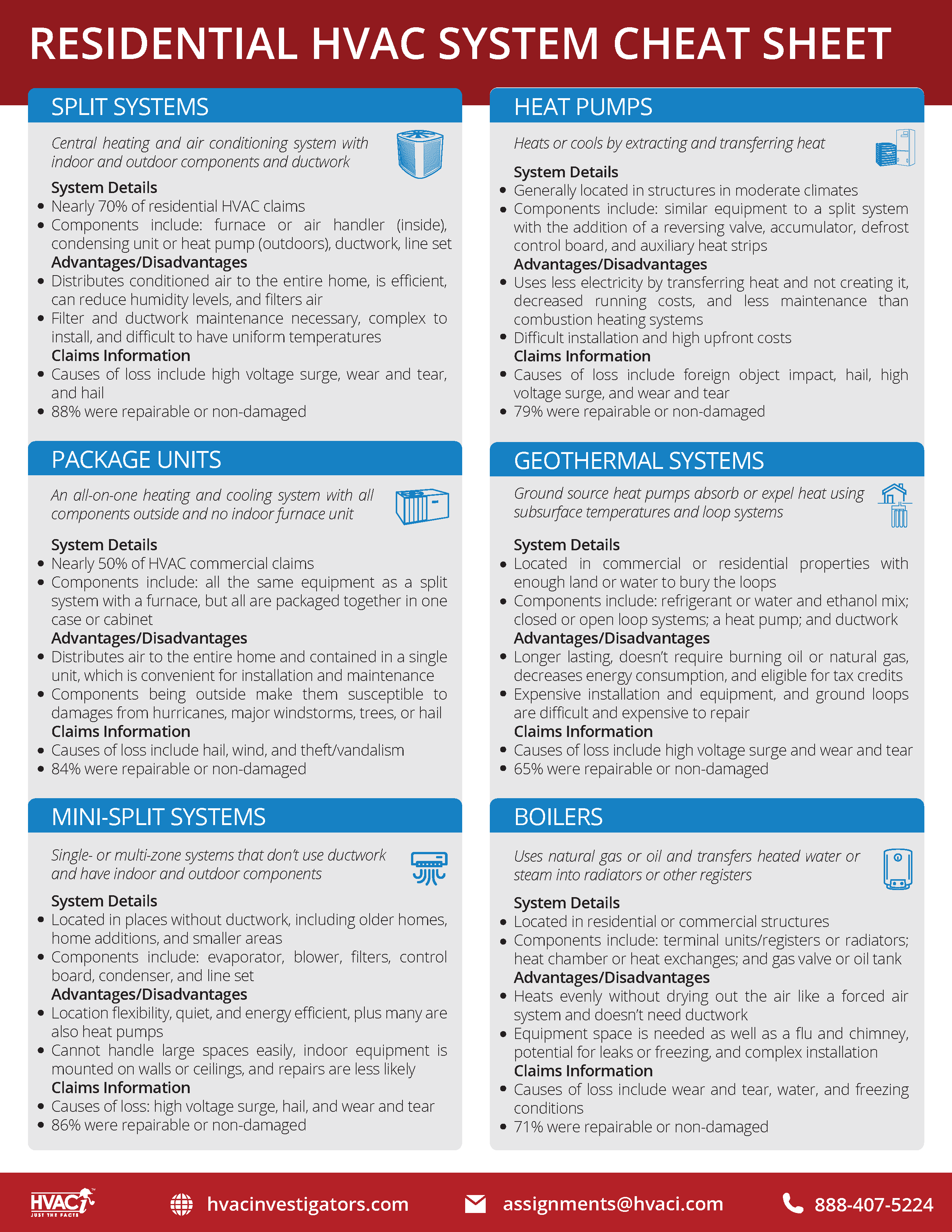

What makes a mini-split system different from a split system? What is an advantage of a boiler compared to a forced air system? What perils frequently cause loss for heat pumps? No need to wonder or spend a lot of time researching. Our Residential HVAC System Cheat Sheet puts this information, and more, all in one go-to reference page.

Fill out the form to receive our guide with brief overviews of split systems, heat pumps, package units, geothermal systems, mini-split systems, and boilers. This one resource will provide you with system details, claims information, and benefits and drawbacks for each to refer to when handling HVAC claims.

What makes a mini-split system different from a split system? What is an advantage of a boiler compared to a forced air system? What perils frequently cause loss for heat pumps? No need to wonder or spend a lot of time researching. Our Residential HVAC System Cheat Sheet puts this information, and more, all in one go-to reference page.

Fill out the form to receive our guide with brief overviews of split systems, heat pumps, package units, geothermal systems, mini-split systems, and boilers. This one resource will provide you with system details, claims information, and benefits and drawbacks for each to refer to when handling HVAC claims.

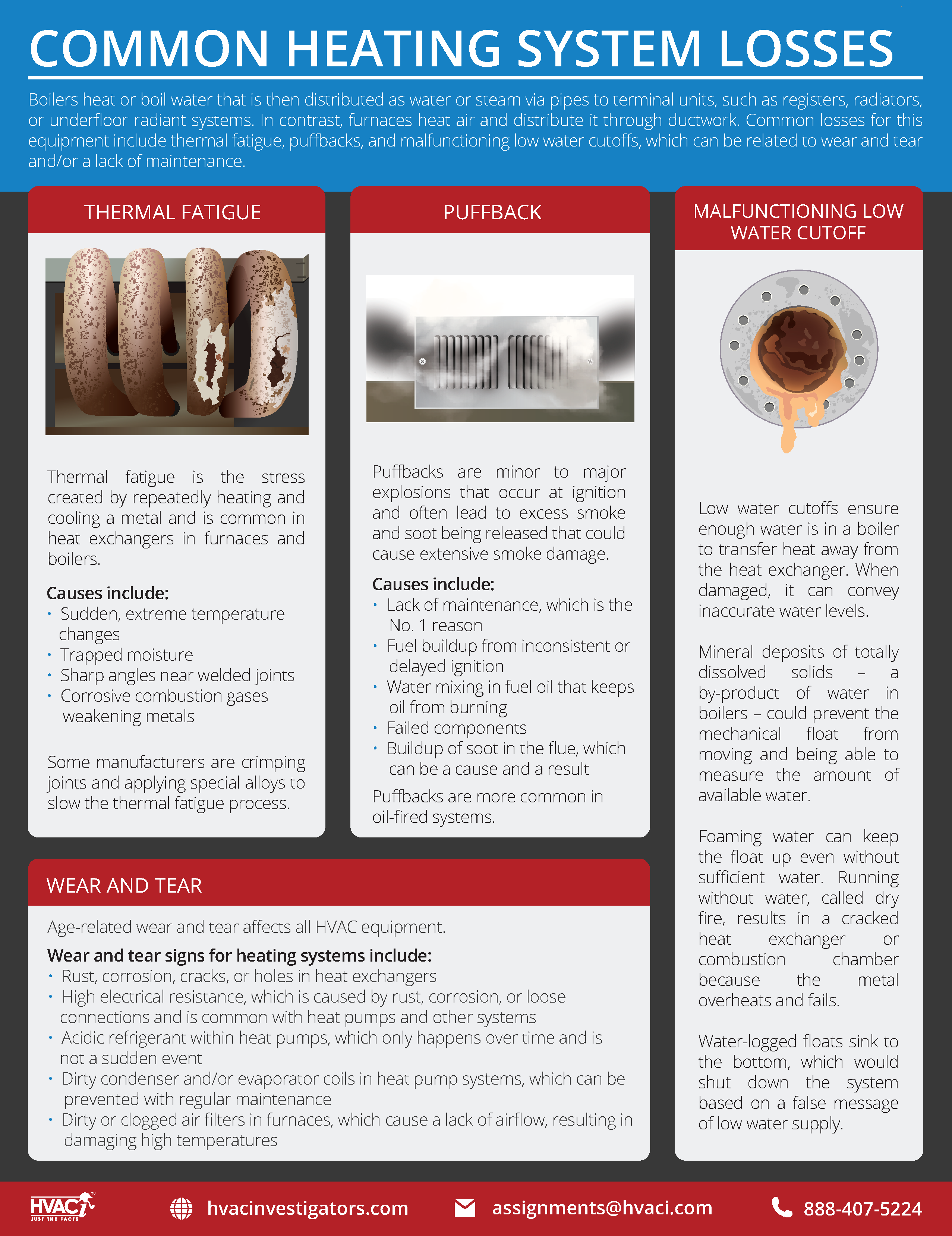

Each cold season policyholders head to their thermostats to get warmer temperatures in their homes and businesses. Working that hard can take a toll on furnaces, boilers, and other heating system components, leading to damages over time that can cause a bigger problem.

The Common Heating System Losses guide delves into a few of the damages heating systems sustain, including thermal fatigue, puffbacks, malfunctioning low water cutoffs, and wear and tear. Read about what these losses are, what causes them, and how to tell if they occurred by filling out the form.

Each cold season policyholders head to their thermostats to get warmer temperatures in their homes and businesses. Working that hard can take a toll on furnaces, boilers, and other heating system components, leading to damages over time that can cause a bigger problem.

The Common Heating System Losses guide delves into a few of the damages heating systems sustain, including thermal fatigue, puffbacks, malfunctioning low water cutoffs, and wear and tear. Read about what these losses are, what causes them, and how to tell if they occurred by filling out the form.

You go through your claims that need to be settled, and there it is – an HVAC system that’s different than the type you are familiar with. Now what?

Adjusters won’t be concerned about whether they’ll make an accurate settlement decision for claims with HVAC equipment if they abide by the following simple steps.

1. Contact the insured immediately.

Reach out to the insured as soon after receiving the claim as possible. It seems simple, but it’s the best way to get the process officially started and to begin obtaining necessary information. Plus, it’s good customer service. Your policyholders know you’re aware of the claim and are going to do whatever it takes within the confines of the policy to return them to pre-loss condition.

2. Gather the details of the claimed equipment.

Knowing the age, brand, and other characteristics of the damaged equipment will be important while settling an HVAC claim.

You’ve made a connection with the policyholder. Take the time to get the details of the equipment that’s being claimed. Having information such as its brand, estimated age, and system type will be necessary further in the process when verifying that the repair or replacement options are compatible to the rest of the components and are of Like Kind and Quality (LKQ).

If your insured doesn’t know those details, don’t worry just yet. These can be obtained during the testing phase.

3. Review what the contractor and policyholder submitted to have a better handle on potential damages and what settlement is being requested.

Contractors may recommend full replacements of HVAC systems without first proving cause of loss and scope of damage – both of which affect settlements.

Policyholders and contractors may provide more information for some claims than others. Key elements to note are if your policyholders are claiming a full HVAC system replacement, if they provided a cause of loss, if the damage is typical for the age of the equipment, or if there really isn’t a lot for you to go on. You wouldn’t want to settle a claim without doing your own assessments first, but it’s good to know what you or an equipment assessor may be walking into.

4. Choose a qualified expert to evaluate the HVAC equipment.

Whether your policyholder submitted little information or provided a book, it’s important you get the claimed systems checked out for yourself. You don’t have to be an expert on HVAC equipment to be able to make accurate settlements – but the third-party HVAC company you have doing the work should have the experience and knowledge to fully evaluate the components in an objective and timely manner.

Making accurate settlements starts with choosing the right HVAC assessment vendor. For guidance, watch the What to Look for in an HVAC Claims Vendor video.

5. Ensure all HVAC systems and components are assessed.

Make sure no shortcuts are taken when assessing the equipment. Every system, regardless of how many are included on the claim, should be tested. Comprehensive evaluations will determine what components are damaged and the scope of the problem. Sometimes a policyholder won’t know that a different component is causing the issue, or some of the claimed systems will be non-damaged.

It’s important that extra effort is spent to determine the cause of loss and scope of damage so that you are only settling for equipment that is actually damaged and covered by the policy. This will lessen the chance that the claim gets reopened for additional damages in the future.

6. If covered, confirm recommended repairs and replacements are compatible and LKQ.

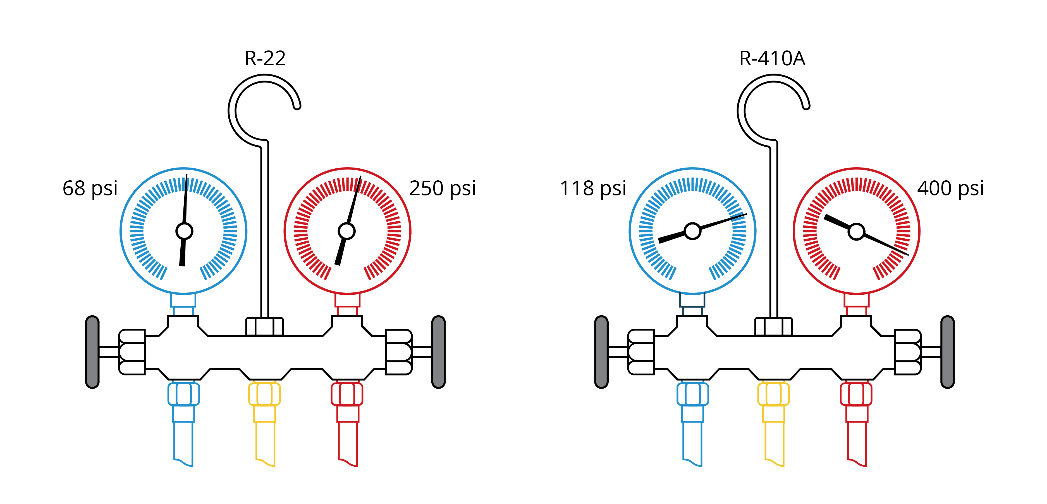

HVAC systems have different types of refrigerant that aren’t interchangeable and have varying constraints, such as the pressure requirements shown here. All equipment needs to be compatible for the policyholder’s system.

HVAC systems may be functioning properly at the time of the assessment, which could lead to a finding of non-damaged. But because of their exposure to the elements and how long some of the components can last, wear and tear is also a common cause of loss, which may not be covered by the policy. Both scenarios could end the claim settlement process.

If the cause of loss is covered, the assessment should have provided recommended next steps, including repair and replacement options. Pull out that information about the policyholder’s current HVAC system. Some components aren’t compatible with certain systems based on the refrigerant used or other factors. Sometimes the replacement options included in the claim, either by a contractor or the policyholder, are unnecessarily better than what was there before. Verify all recommended repair and replacement options are in line with what the policyholder currently has and that it’s LKQ.

7. Confirm the recommended components are available and in line with regulations.

Having a plan of action with recommended repairs and replacements is only as good as how well it can be executed. Make sure items that are needed can be readily purchased by the contractor or policyholder. If your third-party vendor didn’t do this, which it should have, have someone perform a desktop review that can check manufacturer databases for product availability.

The recommended repairs and replacements should be aligned with local and federal regulations. But make sure you clearly understand what they are, even if your policyholder or the contractor doesn’t. One topic that frequently gets misunderstood is the use of R-22 following the phase-out. For a clear understanding of how that comes into play, check out 6 Truths You Should Know About the R-22 Phase-Out When Handling HVAC Claims.

8. Confirm repair and replacement costs are market value.

Sometimes replacements have already been made or you are confident the scope of repairs is appropriate. However, costs can fluctuate depending on the contractor, location, or equipment, and it’s important adjusters confirm they’re in line with market value.

A desktop review can help check for available equipment and verify manufacturer pricing and local labor costs. This ensures the policyholder – and the carrier – is settling for the applicable amount.

9. Keep the policyholder informed about what is happening with the claim at each step.

Each claim has a lot of moving parts, but it’s critical policyholders are kept in the loop about where it is in the process. This makes for a better insured experience and shows you care about your customer and their claim.

More importantly, don’t shy away from telling them news you don’t think they want to hear. Do it quickly and be upfront so your policyholder can figure out next steps.

10. Make sure you settle the claim quickly while staying accurate and objective and providing a good policyholder experience.

That sounds like an impossible task – accuracy, objectivity, speed, and a good policyholder experience? Your policyholder shouldn’t have to choose which they get. Following these steps will guarantee that happens, but you don’t have to do them alone. HVACi can help. We provide comprehensive assessments for all HVAC system types with reports that include repair and replacement recommendations with available components priced at market value.

Trust the nation’s leading HVAC and Refrigeration assessment company to keep you one step ahead in making faster and accurate decisions without sacrificing on quality or policyholder experience. Submit a claim to HVACi to find out how it works.

5 Questions to Ask Before Settling HVAC Claims Guide

The simple act of crossing items off your to-do list is a great feeling, particularly if it means you’ve resolved a claim for your insured. But every so often the policyholder has a concern that warrants giving it another look. In this edition of Scary Story, an adjuster needed support evaluating three HVAC systems for the initial claim. A few weeks later, the policyholder was worried about a noise coming from a furnace in one of the systems and wondered if it was related.

Fill out the form to find out why it was such a good idea the adjuster sought help in determining if there was damage and its scope – both times.

Boilers have a variety of equipment used to heat water or steam that is transferred via pipes and terminals, including radiators and non-electric baseboard registers, to warm a home or business.

Boilers have a variety of equipment used to heat water or steam that is transferred via pipes and terminals, including radiators and non-electric baseboard registers, to warm a home or business. Low water cutoffs can be clogged by Total Dissolved Solids in the supply water, which could cause them to send wrong messages to the boiler and either run without an adequate water supply or shut off unnecessarily.

Low water cutoffs can be clogged by Total Dissolved Solids in the supply water, which could cause them to send wrong messages to the boiler and either run without an adequate water supply or shut off unnecessarily. Lightning and high voltage surges are among the perils that can damage a boiler system’s electrical components, including the thermostat.

Lightning and high voltage surges are among the perils that can damage a boiler system’s electrical components, including the thermostat. Boilers have gas valves and burner assemblies that are among the equipment that can be damaged when submerged by water.

Boilers have gas valves and burner assemblies that are among the equipment that can be damaged when submerged by water.

Knowing the age, brand, and other characteristics of the damaged equipment will be important while settling an HVAC claim.

Knowing the age, brand, and other characteristics of the damaged equipment will be important while settling an HVAC claim. Contractors may recommend full replacements of HVAC systems without first proving cause of loss and scope of damage – both of which affect settlements.

Contractors may recommend full replacements of HVAC systems without first proving cause of loss and scope of damage – both of which affect settlements. HVAC systems have different types of refrigerant that aren’t interchangeable and have varying constraints, such as the pressure requirements shown here. All equipment needs to be compatible for the policyholder’s system.

HVAC systems have different types of refrigerant that aren’t interchangeable and have varying constraints, such as the pressure requirements shown here. All equipment needs to be compatible for the policyholder’s system.