A major wildfire taking place close to a residence is a plausible reason for ductwork to become dirty and need replacement. But it’s important an adjuster takes the time to confirm cause of loss.

Fill out the form to receive your copy of the Wildfire Claim Case Study to read about the results of our inspection and recommendations. It will prove why adjusters should always call for an objective and knowledgeable second opinion to review complex equipment before they make settlement decisions.

Even taken literally, “Where there’s smoke, there’s fire” doesn’t always apply when talking about HVAC systems. If flames are across the room, smoke still has a way of traveling into places your policyholder may not notice. One of the prime locations is ductwork in commercial and residential HVAC systems, which could lead to additional concerns. And, though rarer, HVAC equipment could also ignite a fire.

Our guide covers both scenarios to ensure you have what you need to settle claims related to smoke and fire and HVAC systems. We outline six ways this peril could affect equipment, from the ductwork to the motors, and give a short overview of eight components that are most likely to start a fire and why.

Fill out the form to receive your guide for smoke and fire damage to HVAC systems to refer to when settling these kinds of claims.

Having a policyholder take pictures and provide data can be helpful when circumstances don’t allow experts to come in to conduct the evaluation. It can be problematic, however, if the policyholder isn’t asked for all the information at one time or if the adjuster doesn’t know how to interpret the images once they are obtained.

This edition of Scary Story chronicles how one adjuster put the policyholder in a potentially dangerous situation and could have caused further damages based on inaccurate recommendations. Fill out the form to receive your Scary Story: Unhappy Customer guide to find out what happened and how it could have been avoided.

Want more scary stories of real-life claims gone wrong?

A major news outlet described one hurricane as “the strongest storm on the planet right now” while it approached the United States from the Central Pacific area during the 2020 hurricane season. At the time, the storm was a Category 3 with winds of 115 miles per hour. While the headline may have been true for that moment, the strength of hurricanes in the Atlantic Basin has surpassed that many times since 2000, and their severity has been on the incline. From 2000 until present day, there have been 13 Category 5 storms, the strongest on the Saffir-Simpson Hurricane Wind Scale with a maximum sustained wind of 157 miles per hour or greater.

More hurricanes mean more catastrophic storms and losses adjusters will have to settle claims on. Here are the top 5 worst hurricane seasons in the Atlantic Basin since 2000, chosen by the number and severity of the storms.

No. 5 The 2008 Hurricane Season

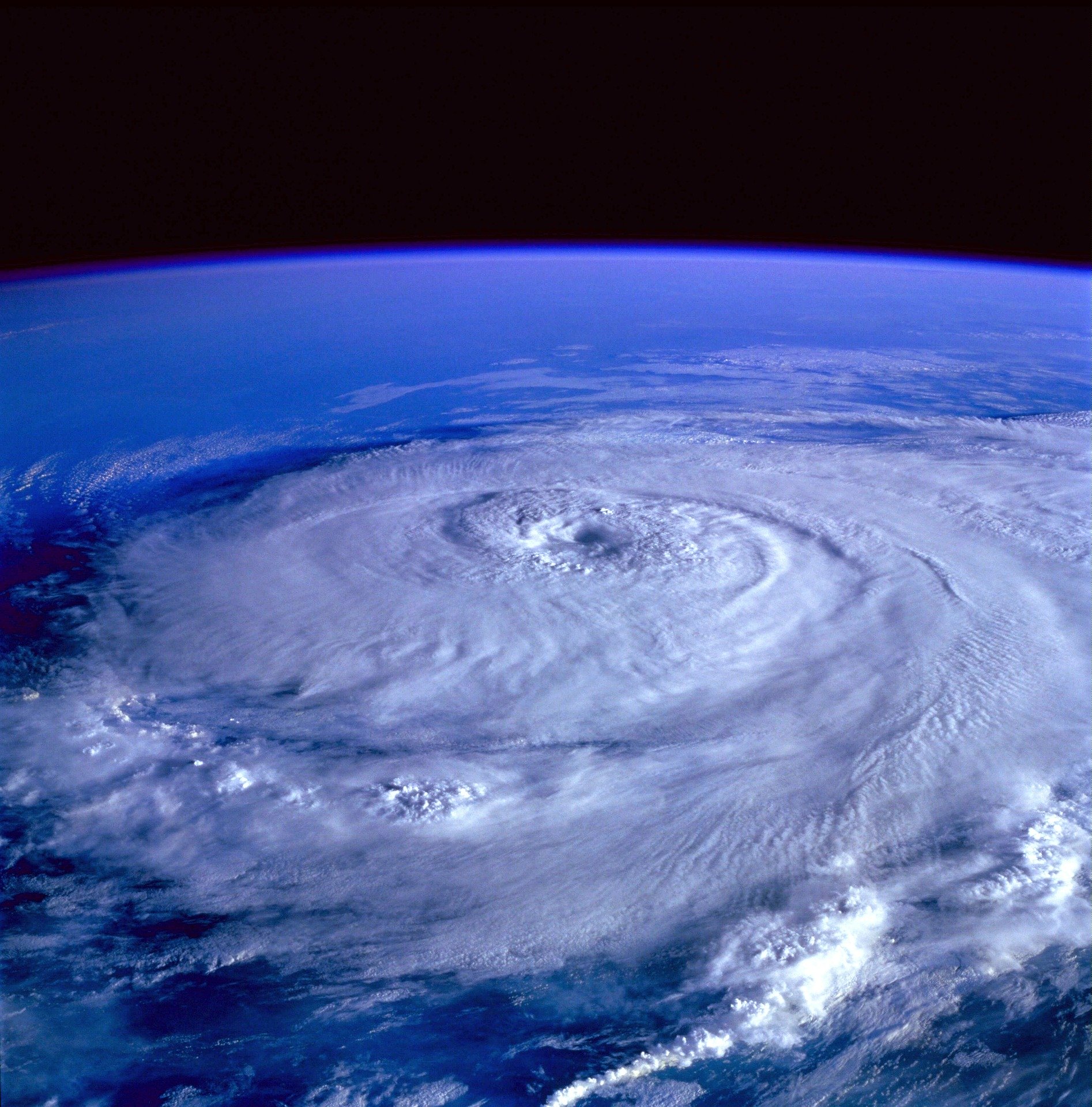

This NASA image of Hurricane Ike was created by Jesse Allen, using data provided courtesy of the MODIS Rapid Response team. Photo Credit: Earth Observatory

The 2008 hurricane season packed a punch with 16 named storms, including 8 hurricanes with 5 major tropical cyclones of Category 3 or higher, according to the StormFax Weather Almanac. It’s the only year on record where a major hurricane took place every month from July to November in the north Atlantic Basin, The National Oceanic and Atmospheric Administration (NOAA) reported. The largest was Hurricane Ike, which the Insurance Information Institute (I.I.I.) recorded as the 7th costliest hurricane in the United States, costing an estimated insured loss of more than $12,400 million in 2008 dollars.

No. 4 The 2010 Hurricane Season

The 2010 hurricane season was described as hyperactive, though no storms made landfall. Photo Credit: “Hurricane” by David Mark / CC BY 4.0

This was the second consecutive season that no hurricane made landfall, but that didn’t make the storms any less intense. StormFax recorded 19 storms, including 12 hurricanes with 5 as a Category 3 or greater. They caused 11 deaths despite none of them reaching the mainland. NOAA described the 2010 season as “hyperactive” because of the number of major storms, though none of them were Category 5. The strength and number of the storms are attributed to the record warm Atlantic Waters, favorable winds off Africa, and weak wind shear aided by La Niña, according to NOAA.

This year marked one of the most active and destructive hurricane seasons on record; although, the first storm didn’t make landfall until August 3. The season ravaged with 15 named storms, including 9 hurricanes and 6 major storms, StormFax reported. These combined for $61 billion in damages and thousands of deaths over several countries, an article from NOAA states. Four out of the nine named storms that hit the continental United States struck Florida. The two strongest storms were Category 5 Hurricane Ivan and Category 3 Hurricane Jeanne. Ivan had sustained winds of 165 miles per hour and hit the Gulf Coast in mid-September. Jeanne caused 3,000 deaths in Hispaniola and later made landfall in Florida with winds topping 120 mph. Hurricane Jeanne caused an estimated $7.5 billion in property damage in the United States, according to the I.I.I.

No. 2 The 2017 Hurricane Season

Hurricane Harvey caused upwards of $20 billion in estimated insured losses in 2017 dollars. Photo Credit: “Hurricane Harvey” by Andrewtheshrew / CC BY 4.0

With Hurricanes Maria, Irma, and Harvey, 2017 holds the record for the first time three Category 4 hurricanes made landfall in the United States and its territories in the same year. Those three storms also were the second, third, and fourth most costly hurricanes in the United States, according to I.I.I. Maria and Irma each caused upward of $30 billion in estimated insured losses, and Harvey caused between $18-20 billion in estimated insured losses in 2017 dollars. The 2017 hurricane season also made a name for itself as the seventh most active season in historical record dating, which goes to 1851. StormFax reported 17 named storms with 10 hurricanes, including 6 major storms.

No. 1 The 2005 Hurricane Season

Hurricane Katrina was the costliest hurricane to ever strike the United States. Photo Credit: “Calamity” by Gabe Raggio / CC BY 4.0

The 2005 hurricane season broke more records than any other year, easily taking the top spot as not only the most active and strongest hurricane season since 2000 – but of all time. StormFax recorded 14 hurricanes and 8 major storms of Category 3 or greater. And there were several greater – including Rita, Wilma, and Katrina. Hurricane Katrina is the costliest hurricane to have ever struck the United States, according to I.I.I., with $41 billion in estimated insured losses in 2005 dollars. It easily overshadowed Hurricane Wilma, which was the ninth costliest hurricane with an estimated $10 billion in insured losses. The 2005 hurricane season exceeded the 1969 record for most hurricanes. There were also 27 named storms formed in 2005, which broke the 1933 record of 21. The 2005 season was the most destructive for the United States, largely due to Hurricane Katrina, and in all, damage estimates are more than $100 billion.

What Does This Mean for Adjusters?

The 2020 hurricane season continues to be predicted as above average for storm activity. From January 1 through July 29, there were eight named storms, which was the most named storms to date in any year since record keeping began in 1851; although, there had only been one hurricane and no major hurricanes. El Niño and La Niña, ocean water temperatures, and weather forecasts, as well as other conditions, make storms ripe for forming, and future hurricane seasons are also likely to continue to be active.

This means the number of large loss claims or ones with high settlements will likely increase. It’s important adjusters have someone they trust to help them with claims, particularly handling accurate and comprehensive assessments to define scope of loss. It’s also essential insurance personnel can confirm cause of loss before assuming a hurricane is to blame for damage and settling for something that shouldn’t have been covered by the policy.

HVACi is here to help adjusters find the answers and better handle claims related to HVAC systems. To learn more about how hurricanes can impact these systems and what to look for, check out our webinar recording for a quick, but comprehensive, overview by our team.

Don’t wait until a hurricane occurs before seeing what HVACi can do for you. Submit a claim and find out how we base our recommendations on just the facts to better equip adjusters to settle claims more accurately.

Geothermal systems offer policyholders a more energy-efficient method of heating and cooling their homes and businesses by taking advantage of natural resources. However, these non-traditional systems could lead to claims being submitted with different kinds of equipment that adjusters aren’t used to working with.

Our one-page Geothermal System Basics guide explores how they work, compares the different types, and notes some of the most frequent perils impacting them. Fill out the form to receive your copy today.

Economizers are required on rooftop package units at residential and commercial properties in some parts of the country because they make HVAC systems more energy efficient. Economizers detect outside temperature and humidity conditions to determine if circulating external air inside will still maintain desired temperatures while lessening how much the HVAC system must work.

Our guide breaks down this complex equipment with the top 5 most important things to know about economizers, including how they work, the different types available, their advantages, why they might fail, and what codes and regulations could impact them. Plus, our labeled internal and external diagrams offer a better understanding of how this equipment works.

Fill out the form to obtain your copy of the guide to reference while handling your next claim that has an HVAC system with an economizer.

If a contractor makes a repair and an HVAC system still doesn’t seem to be working properly, a policyholder and adjuster may take the contractor’s advice and think high-dollar replacement equipment is the next logical step.

Good thing the adjuster didn’t go on that assumption for this commercial claim! Fill out the form to discover the real story about this HVAC system and what HVACi recommended it would take to return it to pre-loss condition.

Economizers, which can be added to the rooftop package units frequently used at commercial properties, have a variety of sensors and other components to gauge if outdoor temperatures and humidity levels are mild enough to give the traditional HVAC system a break. Outside air is applied instead of mechanical cooling to maintain conditions inside.

These components allow policyholders to reduce their energy consumption, but economizers are also included in claims. Adjusters should know how these components work in case a damper or sensor failure winds up on their desks.

A Sensory Experience

Economizers use a system of sensors and vents to maintain proper temperatures inside using outside air.

Externally, economizers look like stacked vents attached to the outside of a rooftop package unit. But multiple components make up this equipment, including the sensors that read temperature, heat, and humidity levels, and the dampers that regulate how much air is let in or out. Enthalpy economizers regulate the use of outside air based on the enthalpy, the amount of internal energy within a system combined with the product of its pressure and volume.

Types of Economizers:

Dry Bulb Economizers: Sensors detect if outdoor air is a certain temperature, which will then open a damper to allow outdoor air in. But there isn’t detection for humidity, which could make for unfavorable conditions inside.

Single Enthalpy Economizer: Sensors determine if the humidity and heat levels are below presets before using outdoor air to cool a building.

Differential Enthalpy Economizer: Two sensors measure indoor and outdoor air enthalpy, and dampers ensure optimum and lowest enthalpy is achieved.

Integrated Differential Enthalpy Economizer: Sensors track return and outdoor air enthalpy, plus there are controls that communicate with an indoor thermostat. If the outdoor air’s temperature and enthalpy are low enough, cooling will start with the economizer, and if not, the compressor will cool the structure.

Economizing Policyholders’ Energy Consumption

The largest advantages of an economizer are reductions in energy consumption and the cost of maintaining the temperature in a commercial building.

According to Powerhouse Dynamics, a single rooftop unit compressor for a small commercial building can draw 5 kilowatt (kW) while it’s running, costing several thousand dollars a month in warmer months. The fan draws only several hundred watts to 2kW, so the cost to cool a building when the compressor is off is cut in half, which can lead to a larger annual savings.

When outside air can be used instead of the traditional cooling methods, the HVAC system doesn’t have to work as hard, which is a benefit to the system itself. Condensing units work less, which reduces maintenance costs, wear and tear, and breakdowns. This could lead to longer system lifespans.

Another advantage is that air quality is improved because of increased ventilation. It is no longer the same air being conditioned and recycled in a facility, but rather, new air from outside is used. Some of the controllers will aid in bringing in the required amount of fresh air and modulate building pressure. To do so, they can have manual or adjustable fixed dampers.

Keep Moisture Out of It, But Follow the Code

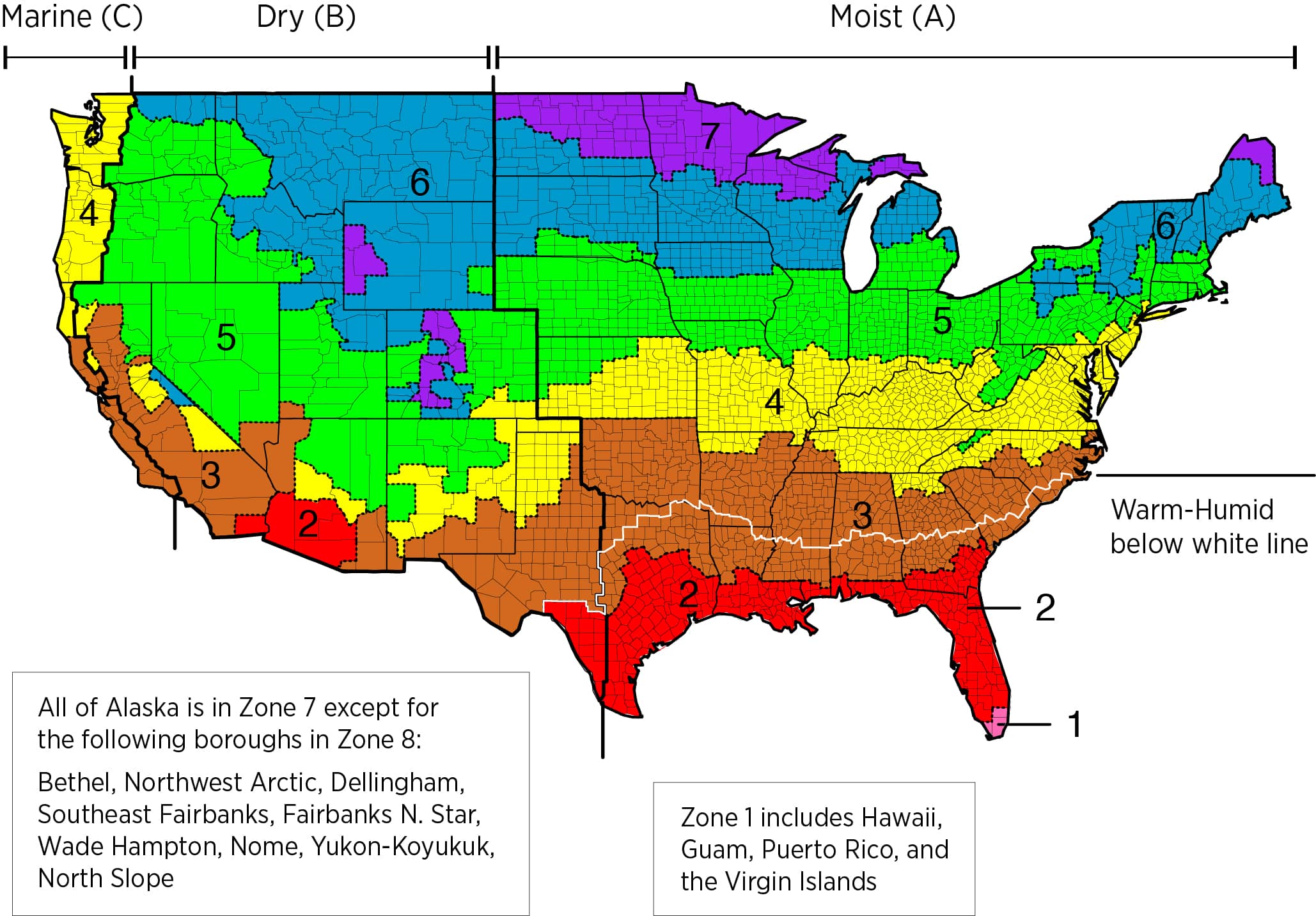

The International Energy Conservation Code’s Climate Zone Map is one of the factors that decides if a commercial facility is required to have an economizer. Photo By: 2012 International Energy Conservation Code

Climates may dictate if economizers are a good choice for a policyholder. Those that are humid and hot are typically not ideal for economizers because the outside air may rarely be cool enough or dry enough to be good for inside.

Climate zones, which denote how warm or dry an area is, are considered in codes and requirements about economizers. Florida, Hawaii, and Puerto Rico are too hot and muggy, so they are exempt from economizer rules because of a lack of energy savings. Having that moist air could increase a policyholder’s risk for mold and mildew, according to Buildings.com, but there are stipulations on where economizers must be used.

According to C403.5 of the International Energy Conservation Code, among the reasons an air or water economizer should be provided are if the individual fan system has a “cooling capacity greater than or equal to 54,000 Btu/h (4.5 ton) in buildings having other than a Group R occupancy.” Group R relates to places providing overnight accommodations, including houses, apartments, and hotels. The total supply capacity of fan cooling units not provided with economizers shouldn’t exceed 20% of the total supply capacity of all fan cooling units in the building or 300,000 Btu/h (25 ton), whichever is greater. Economizers should also be installed on “individual fan systems with cooling capacity greater than or equal to 270,000 Btu/h (22.5 tons) in buildings having a Group R occupancy. The total supply capacity of all fan cooling units not provided with economizers shall not exceed 20% of the total supply capacity of all fan cooling units in the building or 1,500,000 Btu/h (125 ton), whichever is greater.”

Economizers are not required if the individual fan system is not served by chilled water for buildings located in specific climate zones or when 25% of the air designed to be supplied by the system is to spaces not designed to be humidified about 35 degrees Fahrenheit dew-point temperature, if the systems won’t operate more than 20 hours a week, and if the systems are for supermarket areas with open refrigerated casework, among other exceptions.

Adjusters should check if their policyholders are required to have an economizer when handling a claim related to an HVAC system.

Difficulty Detecting Damages

Economizers can sustain similar damages to other outdoor package unit components. This one had foreign object impact.

Economizers typically bring in outside air when conditions are appropriate; otherwise, the standard HVAC system is used. This may make it difficult to know if an economizer is malfunctioning without active monitoring.

Among the damages that can occur are that the sensors can fail or fall out of calibration or other components that detect the condition of the air could have a problem. One damage that might be more noticeable is if a damper is physically stuck, which could keep outside air flowing in even when it shouldn’t. This could be caused by an actuator or linkage failure, which are common. Economizers are usually open about 10%, which can also affect costs. Vents or outside components may sustain damage from hail, foreign object impact, or other perils from being outdoors.

Building codes require some fault detection and diagnostics systems, including refrigerant pressure sensors and a unit control that is configured to provide system status, among others.

Problems could also start before an economizer is ever used. According to a Washington State University Extension Energy Program report about checking economizer operation, nearly 50% of new economizer installations have one or more problems that reduce its effectiveness. This means that rather than having a way to minimize energy consumption, it could actually be costing the policyholder more.

It’s important to have an expert in HVAC systems assess the economizer and the other components listed in insurance claims to ensure they are working properly and to keep the system running as efficiently as possible. The team at HVACi can help by using knowledge and experience to provide comprehensive and objective reports that empower adjusters to accurately handle claims related to HVAC systems and their components. To find out more about what is included in the assessments, submit a claim now.

Policyholders can heat and cool their properties in a more efficient way by letting the Earth’s natural subsurface temperatures do most of the work. These systems use a geothermal heat pump and geothermal loops buried below the frost line to condition warmer and cooler air through heat transfer. Because they aren’t as prevalent as other traditional heating and cooling systems, adjusters should understand how these systems work for when they wind up in claims.

What Makes Geothermal Systems Different?

Geothermal systems have underground pipes and a heat pump to use the Earth’s temperature to warm and cool a home or business.

Traditional furnaces and boilers require burning oil or gas in a combustion chamber, but this isn’t necessary in a geothermal system. The Earth maintains a constant average temperature between 50-60 degrees Fahrenheit 20-30 feet underground regardless of weather and temperatures at the surface. This gives geothermal systems the advantage that the amount of energy needed to condition air to be warmer or cooler is roughly the same year-round versus a traditional HVAC system working harder depending on the outside temperatures.

To warm a facility, the fluid inside the geothermal system’s pipes, including water, refrigerant, or antifreeze, increases temperature from the warmer underground rock, soil, or water. A heat exchanger transfers the heat from the fluid to the building’s heating system to warm the air, and the now-cooler fluid returns to the ground to be warmed again. To cool a structure, the heat is taken out of the building and the fluid in the pipes expels the heat while underground.

According to the U.S Department of Energy, geothermal systems can reduce energy consumption by 25-50% compared to traditional air source heat pumps, and geothermal heat pumps reach efficiencies of as much as 600% on the coldest nights. Other advantages of geothermal systems are that they are quieter, have a longer lifespan, and need little maintenance.

Geothermal systems are more expensive, costing around $15,000; however, policyholders will likely recoup that cost in energy savings over the lifespan of the system. Plus, tax credits are possible. A tax credit expired in 2016, but it was reinstated in 2018 and was retroactive. It initially offered 30% of the amount the owner spent to install it, but the tax credit decreased to 26% in 2020 and will decrease to 22% in 2021. After that, the federal tax credit is scheduled to expire unless Congress approves to extend or renew it.

What Types of Claims Will You See This In?

Property characteristics affect where or how geothermal systems may be installed, but they can be used in commercial and residential properties.

Residential systems can be placed on single or multi-family lots, including under lawns or driveways. Homes built with a traditional HVAC system can be retrofitted for geothermal systems using installed ductwork.

Commercial properties may also benefit from the geothermal system’s cost-effectiveness, energy efficiency, and the fact they are more environmentally friendly. It has been used in schools, high rises, government buildings, apartments, and restaurants as well as for agricultural and industrial facilities.

What Are the Different Types of Geothermal Systems?

Two distinct differences in the types of geothermal systems are whether they are closed or open loop and what they are buried in.

Closed loop systems typically have the geothermal loops, which can be plastic pipes, buried in the ground or under water. The fluid inside continuously circulates. A heat exchanger transfers heat between the refrigerant in the heat pump and antifreeze in the pipes. A variation to this is the direct exchange where the refrigerant circulates through copper tubing underground without a heat exchanger and a larger compressor is needed; however, many government regulations prohibit refrigerant being underground because of potential environmental impacts.

Closed loops can be buried horizontally or vertically. Horizontal loops may be more cost-effective for residential properties, particularly for those with enough land. Pipes buried vertically may be better for commercial buildings because the systems would be larger scale, but less land and landscaping are impacted. The holes can be drilled 100-400 feet deep and the pipes are connected at the bottom with a U-bend pipe.

A geothermal system doesn’t always have to be buried in land. A similar process can be completed under water, which may make it the least expensive option. The pond or lake must have an adequate supply so that the pipes can be 8 feet under the surface where water won’t freeze.

Open loop systems require well water or surface water because that is used in place of heat exchange fluid. Instead of being continually used, water returns to the ground as surface discharge once it leaves the building. However, the water supply must be maintained, and policyholders must adhere to discharge rules that are created and enforced by local ordinances, codes, covenants, or licensing requirements.

A hybrid system that uses both underground geothermal systems and an air source heat pump is also possible, and it’s particularly effective in places where cooling is needed more than heating.

Why Do These Systems Fail?

A sump pump failure caused severe water damage to this geothermal system by corroding some of the equipment.

Energy efficiency and longer lifespan are advantages to having a geothermal system, but they do sustain damages like any other system type.

Leaks from the pipes could cause refrigerant to go underground or in the water source. Any water contamination could be harmful to plants or the water supply. This is particularly important in open loop systems, which should be filtered and free from debris.

Another potential concern is the heat exchanger coils could become corroded and stop the component from exchanging heat.

HVACi assessed hundreds of geothermal systems that appeared in property insurance claims in 2019. High voltage surge and wear and tear were the most frequent cause of loss; though, other perils included smoke and fire, freezing conditions, water damage, and unauthorized modifications. In many claims, the system was found to be in proper working condition at the time of assessment.

The average repair cost for geothermal systems claims assigned to HVACi was $1,261 compared to the average total replacement cost of $14,092.

When Should You Get Help Assessing a Geothermal System?

It’s important to always have an expert assess equipment that you aren’t used to dealing with. Most geothermal system claims that were assigned to HVACi were filed with a stated unknown cause of loss. Our staff used their knowledge and experience with these systems to find actual cause of loss and make recommendations for repairs or replacements based on findings. Submit a claim to learn more about our process in supporting insurance carriers and adjusters in handling these and other claims related to HVAC systems accurately, fairly, and quickly.

The Smoke and Fire Claims Webinar has already occurred. You can watch the recording here.

A small kitchen fire, a furnace blaze, or a wildfire raging miles away from a home or business could all have impacts to a policyholder’s HVAC system. Adjusters may not realize all the different components that could be affected and what that could mean for a claim, which is why we’ve put together this webinar to offer a quick, but comprehensive, overview.

During this webinar, we will explore:

Commonly claimed HVAC systems and components

Ways smoke, fire, and heat damages HVAC equipment

How this peril has appeared in real-life claim scenarios

Important: Pre-recorded webinars do not qualify for CE credit.

This NASA image of Hurricane Ike was created by Jesse Allen, using data provided courtesy of the

This NASA image of Hurricane Ike was created by Jesse Allen, using data provided courtesy of the  The 2010 hurricane season was described as hyperactive, though no storms made landfall. Photo Credit: “Hurricane” by David Mark / CC BY 4.0

The 2010 hurricane season was described as hyperactive, though no storms made landfall. Photo Credit: “Hurricane” by David Mark / CC BY 4.0

Hurricane Harvey caused upwards of $20 billion in estimated insured losses in 2017 dollars. Photo Credit: “Hurricane Harvey” by Andrewtheshrew / CC BY 4.0

Hurricane Harvey caused upwards of $20 billion in estimated insured losses in 2017 dollars. Photo Credit: “Hurricane Harvey” by Andrewtheshrew / CC BY 4.0 Hurricane Katrina was the costliest hurricane to ever strike the United States. Photo Credit: “Calamity” by Gabe Raggio / CC BY 4.0

Hurricane Katrina was the costliest hurricane to ever strike the United States. Photo Credit: “Calamity” by Gabe Raggio / CC BY 4.0 Economizers use a system of sensors and vents to maintain proper temperatures inside using outside air.

Economizers use a system of sensors and vents to maintain proper temperatures inside using outside air.

Economizers can sustain similar damages to other outdoor package unit components. This one had foreign object impact.

Economizers can sustain similar damages to other outdoor package unit components. This one had foreign object impact. Geothermal systems have underground pipes and a heat pump to use the Earth’s temperature to warm and cool a home or business.

Geothermal systems have underground pipes and a heat pump to use the Earth’s temperature to warm and cool a home or business. A sump pump failure caused severe water damage to this geothermal system by corroding some of the equipment.

A sump pump failure caused severe water damage to this geothermal system by corroding some of the equipment.